T122 – Los cambios más importantes de la Sexta Publicación de Versión Anticipada de la Primera Resolución de Modificación a la Miscelánea Fiscal para 2020 y sus anexos/ The Most Important Changes of the 6th Advance Publication of the First Resolution to Amend the Miscellaneous Tax Law for 2020 and its Annexes

La Sexta versión anticipada de modificaciones a la Primera Resolución de Modificaciones de la Miscelánea Fiscal (RMF) fue publicada en el portal del SAT.

Si nos apegáramos a la forma de emisión de RMF en años anteriores, nos encontraríamos en la Séptima Resolución de Modificaciones de la Resolución Miscelanea Fiscal para 2020, mismo que consideramos puede crear un ámbito tanto favorable como desfavorable para el contribuyente, ya que depende de la autoridad la emisión de las versiones anticipadas para crear o eliminar derechos otorgados a los contribuyentes, sin haber sido publicadas en el DOF.

Dentro de los cambios más importantes, se contemplan los siguientes:

- Valor probatorio de la contraseña.

- Buzón tributario y sus mecanismos de comunicación para el envío del aviso electrónico.

- Inscripción en el RFC de personas físicas con CURP.

- La e.firma y la contraseña sustituyen a la firma autógrafa del contribuyente.

- Factor de acumulación por depósitos o inversiones en el extranjero.

- Opción de pago en parcialidades del ISR anual de las personas físicas.

- Presentación de avisos para adherirse o finalizar la opción de pago en especie, así como para la declaración anual del ejercicio fiscal de 2019.

- Entrega de las obras de arte propuestas para el pago de los impuestos causados por la enajenación de obras artísticas y antigüedades propiedad de particulares.

- Opción de calcular retenciones sobre los ingresos diarios.

- Entero de retenciones del ISR que deberán efectuar las plataformas tecnológicas.

- Entero de retenciones del IVA que deberán efectuar quienes presten servicios digitales de intermediación entre terceros.

- Declaración informativa de servicios digitales de intermediación entre terceros.

- Momento para dejar de considerar como pago definitivo del ISR la retención efectuada por plataformas tecnológicas.

- Momento para dejar de considerar como definitiva la retención del IVA efectuada por plataformas tecnológicas.

- Ingresos considerados para optar por realizar pagos definitivos.

- Opción de pago de créditos fiscales por concepto.

- Plazo para la presentación de la declaración anual.

- Suspensión de plazos y términos legales.

Al respecto, nos permitimos desarrollar algunos de los aspectos más importantes en estos cambios y se presentan a continuación.

Valor probatorio de la contraseña:

2.2.1. La contraseña CIEC (Clave de Identificación Electrónica Confidencial) es elegida por el contribuyente y se cuenta con la opción de generar o modificar la contraseña en caso de olvidarla o querer modificarla con tan solo contar con la FIEL. En caso de olvidarla, bastaba con enviar un correo electrónico al correo con el que se dieron de alta ante el SAT para restablecer la contraseña.

Como bien sabemos, la contraseña CIEC es un mecanismo que se utiliza para poder acceder a la información fiscal del contribuyente y, de acuerdo con la regla 2.2.1, ahora el SAT podrá requerir información adicional que permita acreditar la personalidad del contribuyente al solicitar la modificación o generación de la contraseña CIEC.

Se tendrá un plazo de 6 días contados a partir de la solicitud de la generación o actualización de la contraseña para proporcionar la información solicitada por parte de la autoridad. La autoridad tendrá 10 días a partir de recibir la información para responder. En caso de acreditar la información adicional requerida, se expedirá un acuse de requerimiento de información adicional relacionada con la situación fiscal y se podrá realizar la modificación requerida.

En caso de no presentar la documentación requerida por la autoridad, se entenderá por no puesta la solicitud de generación o actualización de contraseña.

La solicitud de generación y actualización de la contraseña deberá realizarse de conformidad con la ficha de trámite 7/CFF “Solicitud de generación y actualización de la contraseña”, contenida en el Anexo 1-A.

La solicitud se tendrá por presentada cuando se acredite la identidad del contribuyente con los elementos aportados; en caso contrario, el contribuyente podrá realizar nuevamente su solicitud hasta por un máximo de dos ocasiones adicionales.

Si eres mayor de edad y solo perteneces al régimen de sueldos y salarios e ingresos asimilados a salarios podrás solicitar tu contraseña utilizando SAT ID.

En caso de que la contraseña no registre actividad por un periodo de cuatro años consecutivos, el SAT podrá bloquearla por inactividad. Consecuentemente, el contribuyente deberá realizar nuevamente su trámite de generación de la contraseña a través del Portal del SAT con su e.firma vigente.

Si la persona fallece y se acredita el fallecimiento, también se restringirá el uso de la contraseña. De igual manera, si se encuentra en el alguno de los supuestos previstos en el artículo 17-H Bis del CFF, podrá restringir temporalmente la contraseña hasta que el contribuyente aclare o desvirtúe dicho supuesto.

Buzón tributario y sus mecanismos de comunicación para el envío del aviso electrónico

2.2.7. De acuerdo a esta regla, se sigue exhortando al contribuyente a tener actualizados los medios de comunicación que sean vigentes y correctos, determinando como medio de contacto un correo electrónico y un número de celular para que el contribuyente sea notificado a ambos medios cuando tenga un mensaje en su buzón tributario, ya que el buzón tributario se considera como el medio de contacto bidireccional entre la autoridad y contribuyente; es por ello que se notifica por este medio. En caso de que el contribuyente no tenga el buzón tributario activo, se le procederá a notificar mediante estrados del SAT, pues se presume que el contribuyente no quiere ser localizado mediante buzón tributario.

Inscripción en el RFC de personas físicas con CURP

2.4.6 Las personas físicas que a partir de 18 años de edad cumplidos requieran inscribirse en el RFC, con o sin obligaciones fiscales, podrán hacerlo a través del Portal del SAT siempre que cuenten con el CURP.

Para generar la contraseña se necesitara tener la e.firma y acceder al portal del SAT con los medios electrónicos que dispongan para el contribuyente.

La e.firma y la contraseña sustituyen a la firma autógrafa del contribuyente.

2.8.3.1 Si bien sabemos tanto la e.firma como la contraseña CIEC sustituyen la firma autógrafa del contribuyente, se detalla aún más que las personas físicas que en su declaración anual soliciten la devolución de saldo a favor, deberán observar lo dispuesto en la regla 2.3.2. Dicha regla establece que, si se obtiene un saldo a favor por un importe de $10,001.00 (diez mil un pesos 00/100 M.N.) a $150,000.00 (ciento cincuenta mil pesos 00/100 M.N.), se deberá utilizar la e.firma para firmar la declaración anual de la que se obtiene el saldo a favor, entre otra serie de requisitos detallados en la misma regla 2.3.2.

Factor de acumulación por depósitos o inversiones en el extranjero

3.16.11. El factor de acumulación por depósitos o inversiones en el extranjero al inicio del ejercicio fiscal de 2019 es de 0.0000.

Opción de pago en parcialidades del ISR anual de las personas físicas

3.17.4. Se otorgó la opción de pago en parcialidades del ISR anual. Las personas físicas podrán efectuar el pago hasta en seis parcialidades, mensuales y sucesivas, siempre que dicha declaración la presenten dentro del plazo establecido en la regla 13.2. y el pago de la primera parcialidad se realice dentro de dicho plazo. Los pagos se realizarán de acuerdo a un factor de actualización de acuerdo al plazo elegido para el pago.

Se le disminuirá la primera parcialidad al importe total a cargo y el resultado obtenido se dividirá entre el factor que corresponda al número total de parcialidades elegidas, de acuerdo al siguiente cuadro:

Esta opción de pago quedará deshabilitada en el servicio de Declaraciones y Pagos una vez vencido el plazo a que se refiere la regla 13.2.

En caso de que no se pague alguna parcialidad dentro del plazo señalado en la fracción II de esta regla, los contribuyentes estarán obligados a pagar recargos por falta de pago oportuno.

Habrá que cumplir con la presentación de la declaración anual antes del 30 de junio de 2020 y empezar a realizar los pagos de acuerdo con las parcialidades solicitadas con el factor de actualización. En caso de no realizar el pago señalado como debe, habrá que pagar recargos. Las parcialidades y el factor dependerán del número de meses que utilicemos para dividir el pago de acuerdo con la tabla anterior.

Presentación de avisos para adherirse o finalizar la opción de pago en especie, así como para la declaración anual del ejercicio fiscal de 2019

11.1.12. Para efectos del Artículo Cuarto, fracción I del Decreto, a más tardar el 30 de junio de 2020, los contribuyentes podrán presentar los avisos para adherirse o finalizar la opción de pago en especie a través de correo electrónico a la dirección pagoenespecie@sat.gob.mx, así como su declaración anual correspondiente al ejercicio fiscal de 2019.

Entrega de las obras de arte propuestas para el pago de los impuestos causados por la enajenación de obras artísticas y antigüedades propiedad de particulares

11.1.13. Los contribuyentes que opten por pagar los impuestos federales a su cargo con obras de arte, en términos de la ficha de trámite 1/DEC-2 “Avisos, declaraciones y obras de arte propuestas en pago de los impuestos por la enajenación de obras artísticas y antigüedades propiedad de particulares” contenida en el Anexo 1-A, podrán entregar durante el mes de julio de 2020, con previa cita generada a través del correo pagoenespecie@sat.gob.mx, las obras de arte que hayan propuesto para el pago de los impuestos causados en la declaración anual de 2019, de conformidad con la regla 11.1.12.

Opción de calcular retenciones sobre los ingresos diarios

12.2.6 Las personas morales residentes en México o residentes en el extranjero con o sin establecimiento permanente en el país, así como las entidades o figuras jurídicas extranjeras obligadas a retener y enterar el ISR a los contribuyentes personas físicas con actividades empresariales que enajenen bienes o presten servicios a través de internet, mediante plataformas tecnológicas, aplicaciones informáticas y similares, podrán optar por calcular las retenciones del ISR de cada contribuyente por periodos diarios, aplicando al monto total de ingresos diarios efectivamente percibidos por el contribuyente las tasas de retención.

En el caso de que se efectúen retenciones por periodos distintos al diario, al total de ingresos de dicho periodo, se le aplicará la tabla que corresponda calculada al número de días que contenga el periodo.

Para el cálculo de retenciones de plataformas digitales, hay distintos factores de retención de acuerdo a la actividad realizada, es por ello que primero hay que ubicar la actividad, después el ingreso percibido y seguido la tasa de retención aplicable.

Entero de retenciones del ISR que deberán efectuar las plataformas tecnológicas

Entero de retenciones del ISR que deberán efectuar las plataformas tecnológicas

12.2.7. De acuerdo a las retenciones de ISR, se realizara el pago de retenciones a través de la “Declaración de pago de retenciones del ISR para plataformas tecnológicas” a más tardar el día 17 del mes inmediato siguiente a aquél en el que se hubiera efectuado la retención.

Entero de retenciones del IVA que deberán efectuar quienes presten servicios digitales de intermediación entre terceros

12.2.9. Para efectos de los artículos 1-A BIS, primer párrafo y 18-J, fracción II, incisos a) y b) de la Ley del IVA, los sujetos a que se refieren las citadas disposiciones que presten servicios digitales de intermediación entre terceros realizarán el entero de las retenciones del IVA a través de la “Declaración de pago de las retenciones del IVA para plataformas tecnológicas” a más tardar el día 17 del mes inmediato siguiente a aquél en el que se hubiera efectuado la retención.

Declaración informativa de servicios digitales de intermediación entre terceros

12.2.10. Para efectos de los artículos 1-A BIS, primer párrafo y 18-J, fracción III, de la Ley del IVA, los sujetos que presten servicios digitales de intermediación entre terceros deberán proporcionar al SAT la información de sus clientes enajenantes de bienes, prestadores de servicios u otorgantes del uso o goce temporal de bienes, aun cuando no hayan efectuado el cobro de la contraprestación y el IVA correspondiente a través de la “Declaración Informativa de servicios digitales de intermediación entre terceros” a más tardar el día 10 del mes inmediato siguiente al que corresponda la información.

Momento para dejar de considerar como pago definitivo del ISR la retención efectuada por plataformas tecnológicas

12.3.15. Para efectos de los artículos 113-A, último párrafo y 113-B, fracciones I y II de la Ley del ISR, en caso de que las personas físicas dejen de ubicarse en los supuestos a que se refieren dichas disposiciones, deberán dejar de aplicar lo dispuesto en las mismas a partir del ejercicio inmediato siguiente a aquél en que dejen de reunir los requisitos para considerar como pago definitivo la retención que les efectúe la plataforma tecnológica, aplicación informática y similares, o el pago que efectúen por los ingresos percibidos directamente.

De acuerdo a la Ley del Impuesto Sobre la renta en su artículo 113-A y 113-B, se da la opción de considerar como pago definitivo la retención de ISR enterada. Esto con la finalidad de que las retenciones sean consideradas como definitivas en lugar de provisionales cuando no se exceda del ingreso anual de trescientos mil pesos anuales, así como se deberá estar a los requisitos establecidos en el artículo 113- B en caso de tener ingresos adicionales a plataformas tecnológicas.

Momento para dejar de considerar como definitiva la retención del IVA efectuada por plataformas tecnológicas

12.3.16. Para efectos de los artículos 18-L y 18-M de la Ley del IVA, cuando las personas físicas dejen de ubicarse en los supuestos a que se refieren dichas disposiciones, dejarán de considerar como pago definitivo la retención del IVA efectuada por plataformas tecnológicas, o el pago que efectúen por los ingresos percibidos directamente a partir del ejercicio fiscal inmediato siguiente a aquél en que dejen de ubicarse en los supuestos señalados en las citadas disposiciones.

Ingresos considerados para optar por realizar pagos definitivos

12.3.17. Para efectos del artículo 113-A, último párrafo de la Ley del ISR, en el total de ingresos anuales, se considerarán los obtenidos por enajenación de bienes o prestación de servicios a través de Internet mediante plataformas tecnológicas, aplicaciones informáticas o similares, así como los ingresos que obtengan de los señalados en los Capítulos I y VI del Título IV de la Ley del ISR.

Opción de pago de créditos fiscales por concepto

13.1. Para efectos de los artículos 20, octavo párrafo, 31, primer párrafo y 65 del CFF, los contribuyentes que tengan a su cargo créditos fiscales pendientes de pago, constituidos por varios conceptos correspondientes a contribuciones, aprovechamientos y/o accesorios, podrán optar por pagar cada uno de forma independiente, junto con su actualización y accesorios, siempre que se respete el orden de pago que establece el artículo 20 del CFF.

Para poder optar por esta facilidad, los contribuyentes deberán presentar un caso de aclaración en el Portal del SAT, manifestando el número de la resolución en los casos que proceda, así como los conceptos, ejercicios y periodos que desea cubrir, además del monto de los pagos a realizar desglosando, en su caso, la actualización y accesorios correspondientes.

De ser procedente la solicitud, la autoridad fiscal emitirá respuesta acompañando el FCF (línea de captura).

El pago que se realice a través del FCF (línea de captura) no limita a la autoridad en el ejercicio de sus atribuciones para continuar, en su caso, con el procedimiento administrativo de ejecución respecto de los demás conceptos. La respuesta de la autoridad y el FCF (línea de captura) al no ser resoluciones administrativas no constituirán instancia, ni podrán ser impugnados.

Plazo para la presentación de la declaración anual

13.2. Para efectos del artículo 150, primer párrafo de la Ley del ISR, las personas físicas podrán presentar su declaración anual correspondiente al ejercicio fiscal de 2019 a más tardar el 30 de junio de 2020. Este plazo fue solicitado por autoridades como CONCANACO SERVYTUR por la situación del COVID 19 por la que estamos atravesando a nivel nacional.

Suspensión de plazos y términos legales

13.3. En atención a las medidas extraordinarias del “Acuerdo por el que se establecen las medidas preventivas que se deberán implementar para la mitigación y control de los riesgos para la salud que implica la enfermedad por el virus SARS-CoV2 (COVID-19)” y conforme al artículo Primero del “Decreto por el que se sanciona el Acuerdo por el que se establecen las medidas preventivas que se deberán implementar para la mitigación y control de los riesgos para la salud que implica la enfermedad por el virus SARS-CoV2 (COVID-19)”, ambos publicados en el DOF el 24 de marzo de 2020, se declara lo siguiente:

A) Para efectos del artículo 12 del CFF, se suspende el cómputo de los plazos y términos legales de los siguientes actos y procedimientos que deban realizarse por y ante el SAT, incluyendo aquellos que se realizan por y ante las entidades federativas en términos de los convenios de colaboración administrativa en materia fiscal federal, siempre que no puedan ser realizados por medios electrónicos:

I. Presentación y resolución del recurso de revocación o de inconformidad.

II. Desahogo y conclusión de los procedimientos a que se refieren los artículos 150, 152, 153, 155 y 158 de la Ley Aduanera.

III. Inicio o conclusión del ejercicio de las facultades de comprobación, actos de verificación, así como el levantamiento de las actas que deban emitirse dentro de los mismos.

IV. Presentación o resolución de solicitudes de permiso, autorización, concesión, inscripción o registro, así como el inicio o resolución de los procedimientos de suspensión, cancelación o revocación de los mismos.

V. Realización, trámite o emisión de los actos previstos en los artículos, 27, apartado C, fracción I, inciso a), 34, 34-A, 36, tercer párrafo, 41, 41-A, 42, antepenúltimo párrafo, 46, 46-A, 48, 49, 50, 52, 52-A, 53, 53-A, 53-B, 63, segundo párrafo, 67, 69-D, segundo párrafo, 121, 133-A y 133-F del CFF; 29 y 203 de la Ley Aduanera y 91 de la Ley del ISR.

VI. Presentación, trámite, atención, realización o formulación de las promociones, requerimientos o actuaciones, que deban realizarse en la sustanciación de los actos a que se refieren las fracciones anteriores.

B) De acuerdo con lo dispuesto en el artículo Primero, fracción II, inciso c) del “Acuerdo por el que se establecen acciones extraordinarias para atender la emergencia sanitaria generada por el virus SARS-CoV2”, publicado en el DOF el 31 de marzo de 2020, de manera enunciativa mas no limitativa, los siguientes actos que deban realizarse por y ante el SAT no se encuentran comprendidos en la suspensión de los plazos y términos a que se refiere el apartado A de la presente regla, incluyendo aquellos que se realizan por y ante las entidades federativas en términos de los convenios de colaboración administrativa en materia fiscal federal:

I. La presentación de declaraciones, avisos e informes.

II. El pago de contribuciones, productos o aprovechamientos.

III. La devolución de contribuciones.

IV. Los actos relativos al procedimiento administrativo de ejecución.

V. Los actos relativos a la entrada al territorio nacional y la salida del mismo de mercancías y de los medios en que se transportan o conducen, incluyendo las referentes al cumplimiento de regulaciones y restricciones no arancelarias.

VI. Los servicios de asistencia y orientación al contribuyente, incluidos la inscripción y avisos ante el RFC, que deban realizarse en las ADSC de manera presencial, los cuales se realizarán previa cita registrada en el Portal del SAT.

C. En términos del artículo 28, tercer párrafo, de la Ley Federal de Procedimiento Administrativo, se suspende el cómputo de los plazos y términos legales de los siguientes actos y procedimientos que deban realizarse por y ante el SAT, siempre que no puedan ser realizados por medios electrónicos:

I. Los relativos al cumplimiento del objeto de la Ley Federal para la Prevención e Identificación de Operaciones con Recursos de Procedencia Ilícita, su Reglamento, las Reglas de Carácter General y demás disposiciones que de estos emanen, incluido la presentación y resolución del recurso de revisión a que se refiere el artículo 61 de dicha Ley.

II. El inicio y conclusión de la verificación en el seguimiento y cumplimiento de los Programas de Auto Regularización, previstos en el transitorio Décimo Cuarto de la Ley de Ingresos de la Federación para el ejercicio 2019 y las disposiciones SEXTA y OCTAVA de las Disposiciones de Carácter General que Regulan los Programas de Auto Regularización, publicadas en el DOF el 16 de abril de 2019, así como la presentación y resolución de las solicitudes a que refieren dicho precepto y disposiciones.

III. Presentación y resolución de las promociones, requerimientos o actuaciones que deban realizarse en la sustanciación de los procedimientos establecidos en los artículos 18, 23 y 25 de la Ley Federal de Responsabilidad Patrimonial del Estado, incluso la presentación y resolución del recurso de revisión correspondiente.

IV. Inicio y resolución del procedimiento a que se refieren las cláusulas Trigésima Cuarta y Trigésima Quinta de los convenios de colaboración administrativa en materia fiscal federal.

V. Presentación, trámite, atención, realización, sustanciación o formulación de las promociones, requerimientos o actuaciones que deban realizarse en la sustanciación de los actos y procedimientos a que se refieren las fracciones anteriores. La suspensión de plazos y términos a que se refiere la presente regla comprenderá del 4 al 29 de mayo de 2020. Tratándose de los plazos que se computen en meses o en años al cómputo de los mismos, se adicionarán 26 días naturales, al término de los cuales vencerá el plazo de que se trate. En caso de que alguno de los actos o procedimientos cuyo plazo se suspende conforme a la presente regla se realice durante el periodo de suspensión previsto en la misma, dicho acto se entenderá efectuado el primer día hábil del mes de junio de 2020.

Fuente:

SEXTA VERSIÓN ANTICIPADA DE PRIMERA RESOLUCIÓN DE MODIFICACIONES A LA RESOLUCIÓN MISCELÁNEA FISCAL PARA 2020 Y SUS ANEXOS 1-A, 5, 6, 7, 9, 14 Y 23

“En TLC Asociados desarrollamos un equipo multidisciplinario de expertos en auditorías y análisis de riesgos para asesorar, implementar estrategias y dar cumplimiento en operaciones de comercio exterior”.

Para más información o comentarios sobre esta publicación contacte a:

División de Impuestos Corporativos

TLC Asociados S.C.

Prohibida la reproducción parcial o total. Todos los derechos reservados de TLC Asociados, S.C. El contenido del presente artículo no constituye una consulta particular y por lo tanto TLC Asociados, S.C., su equipo y su autor, no asumen responsabilidad alguna de la interpretación o aplicación que el lector o destinatario le pueda dar.

The 6th advanced version of modifications to the First Resolution to amend the Miscellaneous Tax Law (RMF for its Spanish acronym) was published in the SAT website.

If we follow the form in which the RMF was issued in previous years, we would now be in the Seventh Resolution of Amendments for the 2020 Miscellaneous Tax Resolution, which we believe may create both a favorable and unfavorable environment for the taxpayer, since it is up to the authority to issue the advance versions to create or suppress rights granted to the taxpayers, without having to be published in the Official Journal of the Federation.

Some of the most important changes are:

- Password probative value.

- Tax mailbox and its communication mechanisms for sending electronic notice.

- Registration of natural persons with CURP to the RFC.

- The electronic signature and the password replace the taxpayer’s physical signature.

- Accumulation factor for deposits or investments abroad.

- Option to pay the annual income tax of natural persons in installments.

- Submission of notices to join or terminate the payment in kind option, as well as for the annual return for the 2019 tax year.

- Delivery of works of art proposed for payment of taxes caused by the sale of works of art and antiques owned by private individuals.

- Option to calculate withholdings on daily income.

- Full income tax withholdings made by technology platforms.

- Full VAT withholding to be done by those providing digital intermediary services between third parties.

- Information statement on digital intermediary services between third parties.

- Moment to stop considering the withholding made by technological platforms as a definitive payment of the income tax.

- Moment to stop considering as definitive the VAT withholding made by technology platforms.

- Income considered for making final payments.

- Tax credit payment option.

- Deadline to submit the annual return.

- Suspension of deadlines and legal terms.

In this regard, we expose some of the most important aspects regarding these changes.

Password probative value:

2.2.1. The taxpayer can choose their CIEC password (Confidential Electronic Identification Code) with the option to generate or modify the password if it were to be forgotten or wished to be changed, using he FIEL (electronic signature). If the password is forgotten, all you had to do was send an e-mail to the address you were registered with the SAT to reset your password.

As we know, the CIEC password is a mechanism used to access the taxpayer’s tax information and, in accordance with Rule 2.2.1, the SAT may now require additional information to prove the taxpayer’s identity when requesting the modification or generation of the CIEC password.

There will be a period of 6 days from the request to generate or update the password for providing the information requested by the authority. The authority will have 10 days from receiving the information to respond. In case of proof of the additional information required, an acknowledgement of request for additional information related to the tax situation will be issued and the required modification may be made.

Failure to provide the documentation required by the authority will result in a failure to generate or update a password.

The request for generation and update of the password must be made in accordance with the processing form 7/CFF “Request for generation and update of the password”, contained in Annex 1-A.

The request shall be deemed to have been submitted when the identity of the taxpayer is proven with the elements provided; otherwise, the taxpayer may make the request again up to a maximum of two additional times.

If you are of legal age and only belong to the system of wages and salaries and income assimilated to wages you can request your password using SAT ID.

If your password does not register activity for a period of four consecutive years, the SAT may block it for inactivity. Consequently, the taxpayer will have to carry out the password generation process again through the SAT Portal with his or her current signature.

If the person dies and the death is accredited, the use of the password will also be restricted. Similarly, if the taxpayer is in any of the cases contemplated in Article 17-H Bis of the CFF, the password may be temporarily restricted until the taxpayer clarifies or denies such case.

Tax mailbox and its communication mechanisms for sending electronic notice

2.2.7. According to this rule, the taxpayer is still encouraged to have updated the means of communication that are in force and correct, determining as a means of contact an e-mail and a cell phone number so that the taxpayer is notified to both means when he has a message in his tax mailbox, since the tax mailbox is considered as the two-way means of contact between the authority and the taxpayer; that is why he is notified by this means. In case the taxpayer does not have an active tax mailbox, he will be notified through the SAT, since it is presumed that the taxpayer does not want to be located through the tax mailbox.

Registration of natural persons with CURP to the RFC

2.4.6 Individuals over 18 years of age who require registration in the RFC, with or without tax obligations, may do so through the SAT Portal provided they have the CURP.

In order to generate the password, it will be necessary to have the e-signature and access the SAT portal with the electronic means available to the taxpayer.

The electronic signature and the password replace the taxpayer’s physical signature

2.8.3.1 While we know that both the electronic signature and the CIEC password replace the autograph signature of the taxpayer, it is even more detailed that the individuals who, in their annual declaration, request a refund of the balance in favor of the taxpayer must observe the provisions of Rule 2.3.2. Said rule establishes that if a favorable balance is obtained in the amount of $10,001.00 (ten thousand one pesos 00/100 M.N.) to $150,000.00 (one hundred fifty thousand pesos 00/100 M.N.), the electronic signature must be used to sign the annual return from which the favorable balance is obtained, among other requirements detailed in the same rule 2.3.2.

Accumulation factor for deposits or investments abroad

3.16.11. The accumulation factor for deposits or investments abroad at the beginning of fiscal year 2019 is 0.0000.

Option to pay the annual income tax of natural persons in installments

3.17.4. The option was granted to pay the annual income tax in installments. Individuals may make payment in up to six monthly and successive installments, provided that the return is filed within the period established in Rule 13.2. and the payment of the first installment is made within such period. Payments shall be made according to an updating factor in accordance with the period chosen for payment.

The first instalment shall be reduced to the total amount payable and the result obtained shall be divided by the factor corresponding to the total number of instalments chosen, in accordance with the following table:

| Requested installments | Factor |

| 2 | 0.9875 |

| 3 | 1.9628 |

| 4 | 2.9259 |

| 5 | 3.8771 |

| 6 | 4.8164 |

This payment option will be disabled in the Statements and Payments service after the deadline referred to in rule 13.2.

In the event that any partial payment is not made within the period indicated in section II of this rule, taxpayers shall be obliged to pay surcharges for failure to pay in a timely manner.

The annual declaration must be submitted by June 30, 2020 and payments must be made in accordance with the requested partial payments with the updating factor. If the payment is not made as it should be, surcharges will have to be paid. The installments and factor will depend on the number of months we use to divide the payment according to the table above.

Submission of notices to join or terminate the payment in kind option, as well as for the annual return for the 2019 tax year

11.1.12. For the purposes of Article 4, section I of the Decree, no later than June 30, 2020, taxpayers may submit notices to join or terminate the payment in kind option by e-mail to pagoenespecie@sat.gob.mx, as well as their annual return for the 2019 fiscal year.

Delivery of works of art proposed for payment of taxes caused by the sale of works of art and antiques owned by private individuals

11.1.13. Taxpayers who choose to pay federal taxes on works of art, in accordance with Form 1/DEC-2 “Notices, Declarations and Works of Art Proposed for Payment of Taxes on the Sale of Works of Art and Antiques Owned by Individuals” contained in Schedule 1-A, may deliver during the month of July 2020, with prior appointment generated through the e-mail pagoenespecie@sat.gob.mx, the works of art they have proposed for payment of taxes caused in the 2019 annual return, in accordance with Rule 11.1.12.

Option to calculate withholdings on daily income

12.2.6 Legal entities resident in Mexico or resident abroad with or without a permanent establishment in the country, as well as foreign entities or legal entities obliged to withhold and pay income tax to individuals with business activities that sell goods or provide services through the Internet, by means of technological platforms, computer applications and similar, may choose to calculate the income tax withholdings of each taxpayer for daily periods, applying the withholding rates to the total amount of daily income effectively received by the taxpayer.

In the event that withholdings are made for periods other than the daily period, the corresponding table calculated for the number of days contained in the period will be applied to the total income of such period.

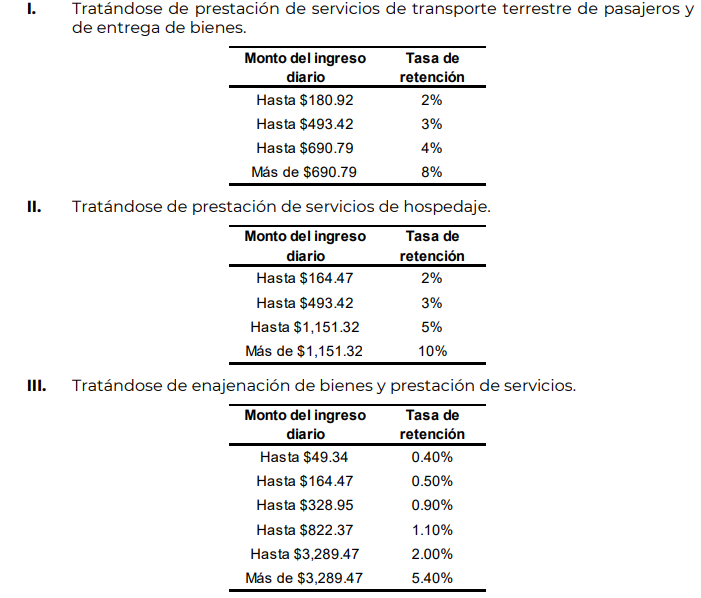

For the calculation of digital platform withholdings, there are different withholding factors according to the activity performed, that is why first the activity must be located, then the income received and then the applicable withholding rate.

I. For land passenger transport services and delivery of goods.

| Daily income | Withholding rate |

| Up to $180.92 | 2% |

| Up to $493.42 | 3% |

| Up to $690.79 | 4% |

| More than $690.79 | 8% |

II. For lodging services

| Daily income | Withholding rate |

| Up to $ 164.47 | 2% |

| Up to $493.42 | 3% |

| Up to $1,151.32 | 5% |

| More than $,151.32 | 10% |

III. For the disposal of goods and provision of services

| Daily income | Withholding rate |

| Up to $49.34 | 0.40% |

| Up to $164.47 | 0.50% |

| Up to $328.95 | 0.90% |

| Up to $822.37 | 1.10% |

| Up to $3,289.47 | 2.00% |

| More than $3,289.47 | 5.40% |

Full income tax withholdings made by technology platforms

12.2.7. According to the income tax withholdings, the payment of withholdings will be made through the “Income tax withholding payment declaration for technological platforms” no later than the 17th day of the month immediately following that in which the withholding was made.

Full VAT withholding to be done by those providing digital intermediary services between third parties

12.2.9. For the purposes of the first paragraph of Article 1-A-AIS and Section II(a) and (b) of Article 18-J of the VAT Act, the persons referred to in the above-mentioned provisions who provide digital intermediary services between third parties shall make the entire VAT withholding through the “Declaration of payment of VAT withholding for technology platforms” no later than the 17th day of the month immediately following the month in which the withholding was made.

Information statement on digital intermediary services between third parties

12.2.10. For the purposes of articles 1-A BIS, first paragraph, and 18-J, section III, of the VAT Law, subjects that provide digital intermediary services between third parties must provide the SAT with information on their clients that sell goods, provide services or grant temporary use or enjoyment of goods, even if they have not collected the consideration and the corresponding VAT through the “Information Statement on Digital Intermediary Services between Third Parties” no later than the 10th day of the month immediately following that to which the information corresponds.

Moment to stop considering the withholding made by technological platforms as a definitive payment of the income tax

12.3.15. For the purposes of the last paragraph of Article 113-A and Sections I and II of Article 113-B of the Income Tax Law, if individuals cease to be in the cases referred to in those provisions, they must cease to apply the provisions thereof as from the fiscal year immediately following that in which they cease to meet the requirements to consider as a definitive payment the withholding made to them by the technological platform, computer application and similar, or the payment made by them for the income received directly.

In accordance with Articles 113-A and 113-B of the Income Tax Law, the option is given to consider as a definitive payment the withholding of income tax paid in full. The purpose of this is to consider the withholdings as definitive instead of provisional when they do not exceed the annual income of three hundred thousand pesos a year, as well as to comply with the requirements established in article 113-B in case of having additional income from technological platforms.

Moment to stop considering as definitive the VAT withholding made by technology platforms

12.3.16. For the purposes of Articles 18-L and 18-M of the VAT Law, when natural persons cease to be in the cases referred to in those provisions, they shall no longer consider as a definitive payment the withholding of VAT made by technological platforms, or the payment made by them for income received directly as from the tax year immediately following that in which they cease to be in the cases referred to in those provisions.

Income considered for making final payments

12.3.17. For purposes of article 113-A, last paragraph of the Income Tax Law, total annual revenues shall include those obtained from the sale of goods or services through the Internet by means of technological platforms, computer applications or similar, as well as the revenues obtained from those indicated in Chapters I and VI of Title IV of the Income Tax Law.

Tax credit payment option

13.1. For the purposes of Articles 20, eighth paragraph, 31, first paragraph and 65 of the CFF, taxpayers who have outstanding tax credits, made up of various items corresponding to contributions, uses and/or accessories, may choose to pay each separately, together with their updating and accessories, provided that the order of payment set out in Article 20 of the CFF is respected.

In order to opt for this facility, taxpayers must submit a case for clarification on the SAT website, stating the resolution number in the appropriate cases, as well as the concepts, fiscal years and periods to be covered, in addition to the amount of the payments to be made, breaking down, if applicable, the corresponding update and accessories.

If the request is appropriate, the tax authority will issue a response accompanied by the FCF (line of capture).

The payment made through the FCF (line of capture) does not limit the authority in the exercise of its powers to continue, if necessary, with the administrative procedure of execution with respect to the other concepts. The response of the authority and the FCF (line of capture) not being administrative decisions shall not constitute an instance, nor may they be contested.

Deadline to submit the annual return

13.2. For the purposes of Article 150, first paragraph of the Income Tax Law, individuals may file their annual return for the 2019 tax year no later than June 30, 2020. This deadline was requested by authorities such as CONCANACO SERVYTUR due to the situation of COVID 19 which we are going through at national level.

Suspension of deadlines and legal terms

13.3. In response to the extraordinary measures of the “Agreement establishing the preventive measures to be implemented for the mitigation and control of health risks implied by the SARS-CoV2 virus disease (COVID-19)” and according to Article One of the “Decree sanctioning the Agreement establishing the preventive measures to be implemented for the mitigation and control of health risks implied by the SARS-CoV2 virus disease (COVID-19)”, both published in the DOF on March 24, 2020, it is stated that:

A. For the purposes of Article 12 of the CFF, the calculation of the legal terms and deadlines of the following acts and procedures that must be carried out by and before the SAT is suspended, including those carried out by and before the federal entities in terms of administrative collaboration agreements on federal tax matters, provided that they cannot be carried out by electronic means:

I. Presentation and resolution of the appeal of revocation or non-conformity.

II. Discharge and conclusion of the procedures referred to in Articles 150, 152, 153, 155 and 158 of the Customs Law.

III. Initiation or conclusion of the exercise of the faculties of verification, acts of verification, as well as the raising of the minutes that should be issued within the same.

IV. Submission or resolution of applications for permits, authorizations, concessions, registrations or inscriptions, as well as the initiation or resolution of procedures for their suspension, cancellation or revocation.

V. Carrying out, processing or issuing of the acts provided for in Articles 27, paragraph C, section I, letter a), 34, 34-A, 36, third paragraph, 41, 41-A, 42, antepenultimate paragraph, 46, 46-A, 48, 49, 50, 52, 52-A, 53, 53-A, 53-B, 63, second paragraph, 67, 69-D, second paragraph, 121, 133-A and 133-F of the CFF; 29 and 203 of the Customs Law and 91 of the Income Tax Law

VI. Presentation, procedure, attention, realization or formulation of the promotions, requirements or actions, that must be carried out in the substantiation of the acts to which the previous fractions refer.

B) In accordance with the provisions of Article 1, Section II, paragraph c) of the “Agreement establishing extraordinary actions to address the health emergency generated by the SARS-CoV2 virus”, published in the DOF on March 31, 2020, the following acts to be performed by and before the SAT are not included in the suspension of the terms and conditions referred to in section A of this rule, including those performed by and before the federal entities in terms of administrative collaboration agreements on federal tax matters:

I. The submission of declarations, notices and reports.

II. The payment of contributions, products or benefits.

III. The return of contributions.

IV. Acts relating to the administrative procedure of execution.

V. The acts related to the entry into and exit from the national territory of goods and the means by which they are transported or driven, including those related to compliance with non-tariff regulations and restrictions.

VI. The assistance and guidance services to the taxpayer, including registration and notices before the RFC, which must be performed at the ADSC in person, which will be performed by appointment registered at the SAT Portal.

C. In terms of article 28, third paragraph, of the Federal Law of Administrative Procedure, the calculation of the legal terms and deadlines for the following acts and procedures to be carried out by and before the SAT is suspended, provided that they cannot be carried out by electronic means:

I. Those relating to compliance with the purpose of the Federal Law for the Prevention and Identification of Transactions with Illegal Provenance Resources, its Regulations, the General Rules and other provisions deriving from them, including the filing and resolution of the appeal for review referred to in Article 61 of that Law.

II. The initiation and conclusion of the verification in the follow-up and compliance with the Self-Regulatory Programs, provided for in the Fourteenth Transitional Provision of the Federal Revenue Law for the 2019 fiscal year and the Sixth and Eighth Provisions of the General Provisions that Regulate the Self-Regulatory Programs, published in the DOF on April 16, 2019, as well as the presentation and resolution of the applications referred to in said provision and provisions.

III. presentation and resolution of the promotions, requirements or actions that must be carried out in the substantiation of the procedures established in articles 18, 23 and 25 of the Federal Law of Patrimonial Responsibility of the State, including the presentation and resolution of the corresponding revision appeal.

IV. Initiation and resolution of the procedure referred to in clauses Thirty-fourth and Thirty-fifth of the administrative collaboration agreements in federal tax matters.

V. Presentation, procedure, attention, realization, substantiation or formulation of the promotions, requirements or actions that must be carried out in the substantiation of the acts and procedures referred to in the previous sections. The suspension of terms and deadlines referred to in this rule shall be from May 4 to 29, 2020. In the case of terms calculated in months or years, 26 calendar days shall be added to the calculation, at the end of which the term in question shall expire. If any of the acts or procedures whose time limit is suspended under this rule are carried out during the period of suspension provided for in this rule, such act shall be understood to have taken place on the first working day of June 2020.

Source:

SIXTH ADVANCE VERSION OF FIRST RESOLUTION OF AMENDMENTS TO THE MISCELLANEOUS TAX RESOLUTION FOR 2020 AND ITS ANNEXES 1-A, 5, 6, 7, 9, 14 AND 23

“In TLC Asociados, we develop a multidisciplinary team of experts in audits and risk analysis for consulting, implementing strategies and complying with foreign trade operations”.

For further information or comments regarding this article, please contact:

Corporate Tax Division

TLC Asociados S.C.