Obligación de emitir CFDI en exportaciones en supuestos donde las mercancías no son objeto de enajenación o son a título gratuito.

I. Planteamiento

“Operaciones de exportación con clave de pedimento A1 incluso las realizadas por empresas IMMEX en las cuales de conformidad con el artículo 29 del Código Fiscal de la Federación se deberá declarar el Comprobante fiscal digital por internet por sus siglas CFDI”.

II. Comentario

1. Derivado de la Reforma del artículo 29 del Código Fiscal de la Federación (en adelante CFF) publicada en el DOF el 8 de diciembre de 2020, a partir del 1 de enero de 2021 es obligatorio emitir un CFDI de Traslado en operaciones de exportación definitiva con clave de pedimento A1 en aquellos supuestos donde las mercancías no son objeto de enajenación o son a título gratuito.

El artículo 29 del CFF establece la obligación de expedir los CFDI por diversos actos o actividades, así como el artículo 29-A del CFF establece los requisitos que deben cumplirse de manera genérica en cualquier CFDI. Asimismo, habrá que atender para este caso en especifico, tanto a la guía del anexo 20 emitida por el SAT como a la guía de llenado del comprobante al que se le incorpore el complemento para comercio exterior para ver especificaciones en el llenado del CFDI.

En relación con la reforma al Código Fiscal de la Federación, se dio a conocer una modificación relacionada con el Comprobante Fiscal Digital por Internet y las operaciones de exportación de mercancías que no sean objeto de enajenación o cuando la enajenación es a título gratuito, que a la letra, señala lo siguiente:

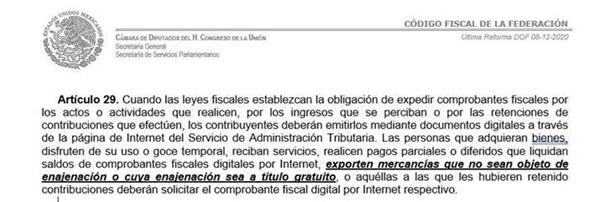

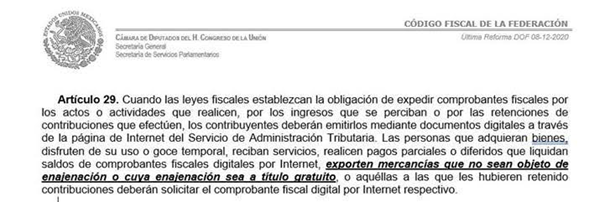

“Artículo 29. Cuando las leyes fiscales establezcan la obligación de expedir comprobantes fiscales por los actos o actividades que realicen, por los ingresos que se perciban o por las retenciones de contribuciones que efectúen, los contribuyentes deberán emitirlos mediante documentos digitales a través de la página de Internet del Servicio de Administración Tributaria. Las personas que adquieran bienes, disfruten de su uso o goce temporal, reciban servicios, realicen pagos parciales o diferidos que liquidan saldos de comprobantes fiscales digitales por Internet, exporten mercancías que no sean objeto de enajenación o cuya enajenación sea a título gratuito, o aquéllas a las que les hubieren retenido contribuciones deberán solicitar el comprobante fiscal digital por Internet respectivo.

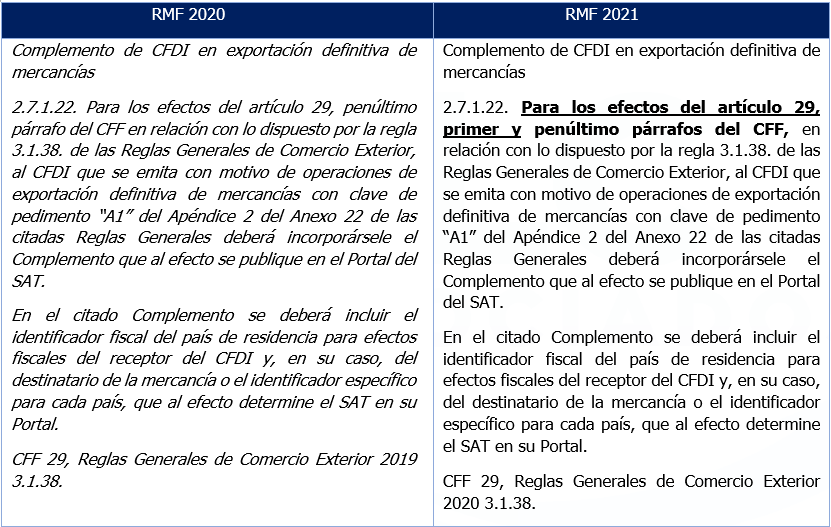

2. La actualización de la nueva regla 2.7.1.22 de la RMF 2021 con respecto de la RMF 2020, únicamente se incorpora el fundamento del primer párrafo del artículo 29 del CFF que refiere al CFDI emitir un CFDI de Traslado en operaciones de exportación definitiva con clave de pedimento A1 en aquellos supuestos donde las mercancías no son objeto de enajenación o son a título gratuito, que corresponde a la reforma del CFF del 8 de diciembre de 2020.

3. La obligación de expedir el CFDI de traslado en exportaciones definitivas para efectos fiscales se sustenta en la regla 2.7.1.22 de la RMF 2021 y, en materia de comercio exterior, en la regla 3.1.38 de las RGCE para 2020.

En términos generales, la regla 2.7.1.22 omite mencionar desde su publicación que la obligación es exclusiva para la “enajenación de bienes en términos del artículo 14 de la CFF” como lo señala la regla 3.1.38 de las RGCE 2020. Por lo tanto, es posible interpretar que es aplicable a supuestos distintos de la enajenación, tal es el caso de las mercancías que no son objeto de enajenación o son a título gratuito.

En este sentido, derivado de la reforma al artículo 29 del CFF y la regla 2.7.1.22 RMF 2021, también se contempla el supuesto emitir un CFDI para las mercancías que no son objeto de enajenación o son a título gratuito.

Cabe mencionar que no ha sido reformada la regla 3.1.38 de las RGCE 2020 para indicar una obligación expresa en las operaciones de comercio exterior.

4. En materia de comercio exterior, es posible emitir un CFDI de Traslado en operaciones de exportación con clave de pedimento “A1” en aquellos supuestos donde las mercancías no son objeto de enajenación o son a título gratuito.

La “Guía de llenado del comprobante al que se le incorpore el complemento para comercio exterior” emitida en el periodo 2020 menciona lo siguiente:

A. Enajenación a título gratuito

En el caso de exportaciones definitivas con la clave de pedimento “A1” en las cuales la mercancía se enajena, pero dicha enajenación se realiza a título gratuito, el contribuyente podrá optar por utilizar cualquiera de los siguientes mecanismos siempre con la versión 1.1 del complemento de comercio exterior:

a) Emitir el comprobante como tipo “I” (Ingreso) en el que se incluya la descripción y el valor mercantil de las mercancías y establezca a continuación un descuento por el mismo monto de estas, de forma que el CFDI resulte con valor “0”, además de incorporarle el complemento, sin incluir el nodo “Propietario” y el campo “Motivo de Traslado”.

b) Emitir el comprobante como tipo “T” (Traslado), e incorporar el complemento que incluya el nodo “Propietario” y el campo “Motivo de Traslado”.

B. No hay enajenación

No obstante, en el caso de exportaciones de mercancías definitivas con clave de pedimento “A1”, cuando no existe enajenación de estas en términos del artículo 14 del CFF, no es obligatorio el usar el complemento para comercio exterior. Los contribuyentes que voluntariamente quieran hacerlo podrán expedir el CFDI conforme al inciso b) descrito en esta sección. En estos casos, no obstante, se deberá seguir cumpliendo con la transmisión del acuse de valor y declarar en el pedimento correspondiente, en el campo “505”, el número de folio fiscal del CFDI, así como el acuse de valor a que se refiere la regla 1.9.18., de las RGCE vigentes.

http://omawww.sat.gob.mx/tramitesyservicios/Paginas/documentos/GuiaComercioExterior3_3.pdf

Sin embargo, en el futuro la autoridad fiscal deberá actualizar este manual de lineamientos para precisar en una nueva guía de llenado, si el CFDI de traslado requiere el Complemento de Comercio Exterior, o bien, seguirá siendo optativo.

5. El Agente Aduanal o la Agencia Aduanal no tienen obligación de verificar el folio del CFDI de Traslado.

En términos de la regla 3.1.39 de las RGCE para 2020, se menciona que, en relación a la regla 3.1.38 de la citada disposición, los agentes aduanales, agencias aduanales o apoderados aduanales deberán verificar que el número o números de folio fiscal del CFDI corresponda al que aparece en el Portal del SAT cuando actúen por cuenta de aquellos, al determinar las contribuciones aplicables. Por lo tanto, no tienen obligación de verificar número o números de folio fiscal del CFDI de Traslado.

6. El Agente Aduanal o la Agencia Aduanal no tienen obligación de digitalizar la impresión del CFDI y el contenido del archivo XML.

La hoja informativa 17 con fecha del 30 de junio de 2016 menciona que en las operaciones que se realicen al amparo de la regla 3.1.35 RGCE 2016, con excepción del segundo párrafo (actualmente 3.1.38 RGCE 2020), deben transmitir el CFDI y XML (Tenga complemento o no) como documento digital en Ventanilla Única, con la etiqueta 170 (Factura o CFDI)

Por lo tanto, no sería aplicable al procedimiento del CFDI de Traslado que establece el artículo 29 CFF y que describe la regla 2.7.1.22 de la RMF para 2020.

https://www.ventanillaunica.gob.mx/vucem/meses/junio2016/hojainfo17.pdf

7. Llenado del CFDI de Traslado

El CFDI de traslado principalmente debe cumplir con todos los requisitos generales del artículo 29-A del Código Fiscal. Así mismo, de acuerdo a la guía del llenado anexo 20 emitida por el SAT y la Guía de llenado del comprobante al que se le incorpore el complemento para comercio exterior Aplicable para la versión 3.3 del CFDI y el complemento para comercio exterior versión 1.1, deberá como mínimo contener lo siguiente:

- Se debe indicar que es un CFDI de traslado (T)

- RFC emisor

- RFC receptor

- Número de folio fiscal

- Domicilio Fiscal

- Concepto conforme catálogo del SAT

- Cantidad conforme catalogo del SAT

- Unidad de medida conforme catálogo del SAT

- XML correspondiente

- Sello digital

- Código QR

- Valor unitario debe ser cero

- Subtotal y total debe ser cero

De acuerdo con la guía de llenado anexo 20 en el concepto de la información, se debe llenar a detalle en qué consiste la mercancía que está siendo transportada.

El tipo de comprobante registrado es “T” (Traslado) y se deben considerar los siguientes puntos:

- Se debe registrar el campo Motivo Traslado

- Si se registra la Clave 05 (envío de mercancías propiedad de terceros) en el campo motivo de traslado, se debe registrar por lo menos un propietario.

- Si se registran las claves 01 (envío de mercancías facturadas con anterioridad), 02 (reubicación de mercancías propias), 03 (envío de mercancías objeto de contrato de consignación) o 04 (envío de mercancías para posterior enajenación), NO se debe registrar el nodo propietario.

En este tipo de comprobante, los siguientes campos no deben existir:

- Condiciones de pago

- Descuento de los conceptos

- El nodo Impuestos Forma de pago

- Método de Pago

- Campo de descuentos

- Retenciones

El CFDI de traslado no releva de acompañar la mercancía con la documentación necesaria para su estancia legal. Se sugiere revisar la guía de llenado anexo 20 y la guía de comercio exterior para su correcta aplicación.

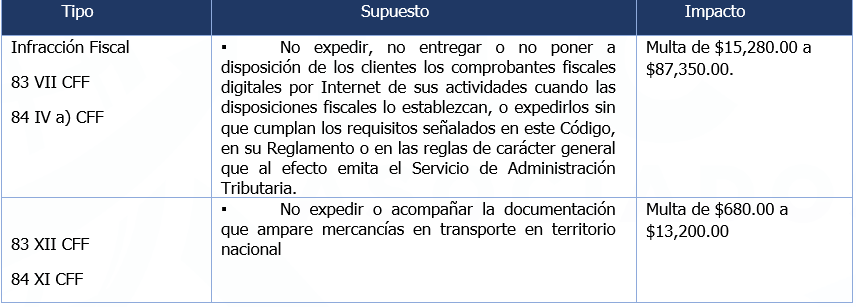

8. Los riesgos fiscales para la empresa IMMEX por no expedir los CFDI de Traslados son las infracciones y sanciones que se indican:

III. Fundamentos

A. Código Fiscal de la Federación

Artículo 14. Se entiende por enajenación de bienes:

I. Toda transmisión de propiedad, aun en la que el enajenante se reserve el dominio del bien enajenado

II. Las adjudicaciones, aun cuando se realicen a favor del acreedor.

III. La aportación a una sociedad o asociación.

IV. La que se realiza mediante el arrendamiento financiero.

V. La que se realiza a través del fideicomiso, en los siguientes casos:

a) En el acto en el que el fideicomitente designe o se obliga a designar fideicomisario diverso de él, siempre que no tenga derecho a readquirir del fiduciario los bienes.

b) En el acto en el que el fideicomitente pierda el derecho a readquirir los bienes del fiduciario, si se hubiera reservado tal derecho.

Cuando el fideicomitente reciba certificados de participación por los bienes que afecte en fideicomiso, se considerarán enajenados esos bienes al momento en que el fideicomitente reciba los certificados, salvo que se trate de acciones.

VI. La cesión de los derechos que se tengan sobre los bienes afectos al fideicomiso, en cualquiera de los siguientes momentos:

a) En el acto en el que el fideicomisario designado ceda sus derechos o dé instrucciones al fiduciario para que transmita la propiedad de los bienes a un tercero. En estos casos, se considerará que el fideicomisario adquiere los bienes en el acto de su designación y que los enajena en el momento de ceder sus derechos o de dar dichas instrucciones.

b) En el acto en el que el fideicomitente ceda sus derechos si entre éstos se incluye el de que los bienes se transmitan a su favor.

Cuando se emitan certificados de participación por los bienes afectos al fideicomiso y se coloquen entre el gran público inversionista, no se considerarán enajenados dichos bienes al enajenarse esos certificados, salvo que estos les den a sus tenedores derechos de aprovechamiento directo de esos bienes, o se trate de acciones. La enajenación de los certificados de participación se considerará como una enajenación de títulos de crédito que no representan la propiedad de bienes y tendrán las consecuencias fiscales que establecen las Leyes fiscales para la enajenación de tales títulos.

VII. La transmisión de dominio de un bien tangible o del derecho para adquirirlo que se efectúe a través de enajenación de títulos de crédito, o de la cesión de derechos que los representen.

Lo dispuesto en esta fracción no es aplicable a las acciones o partes sociales.

VIII. La transmisión de derechos de crédito relacionados a proveeduría de bienes, de servicios o de ambos a través de un contrato de factoraje financiero en el momento de la celebración de dicho contrato, excepto cuando se transmitan a través de factoraje con mandato de cobranza o con cobranza delegada así como en el caso de transmisión de derechos de crédito a cargo de personas físicas, en los que se considerará que existe enajenación hasta el momento en que se cobre los créditos correspondientes.

IX. La que se realice mediante fusión o escisión de sociedades, excepto en los supuestos a que se refiere el artículo 14-B de este Código.

Se entiende que se efectúan enajenaciones a plazo con pago diferido o en parcialidades, cuando se efectúen con clientes que sean público en general, se difiera más del 35% del precio para después del sexto mes y el plazo pactado exceda de doce meses. Se consideran operaciones efectuadas con el público en general cuando por las mismas se expidan los comprobantes fiscales simplificados a que se refiere este Código.

Se considera que la enajenación se efectúa en territorio nacional, entre otros casos, si el bien se encuentra en dicho territorio al efectuarse el envío al adquirente y cuando no habiendo envío, en el país se realiza la entrega material del bien por el enajenante.

Cuando de conformidad con este Artículo se entienda que hay enajenación, el adquirente se considerará propietario de los bienes para efectos fiscales.

Artículo 29. Cuando las leyes fiscales establezcan la obligación de expedir comprobantes fiscales por los actos o actividades que realicen, por los ingresos que se perciban o por las retenciones de contribuciones que efectúen, los contribuyentes deberán emitirlos mediante documentos digitales a través de la página de Internet del Servicio de Administración Tributaria. Las personas que adquieran bienes, disfruten de su uso o goce temporal, reciban servicios, realicen pagos parciales o diferidos que liquidan saldos de comprobantes fiscales digitales por Internet, exporten mercancías que no sean objeto de enajenación o cuya enajenación sea a título gratuito, o aquellas a las que les hubieren retenido contribuciones deberán solicitar el comprobante fiscal digital por Internet respectivo.

Los contribuyentes a que se refiere el párrafo anterior deberán cumplir con las obligaciones siguientes:

I. Contar con un certificado de firma electrónica avanzada vigente.

II. Tramitar ante el Servicio de Administración Tributaria el certificado para el uso de los sellos digitales.

Los contribuyentes podrán optar por el uso de uno o más certificados de sellos digitales que se utilizarán exclusivamente para la expedición de los comprobantes fiscales mediante documentos digitales. El sello digital permitirá acreditar la autoría de los comprobantes fiscales digitales por Internet que expidan las personas físicas y morales, el cual queda sujeto a la regulación aplicable al uso de la firma electrónica avanzada.

Los contribuyentes podrán tramitar la obtención de un certificado de sello digital para ser utilizado por todos sus establecimientos o locales, o bien, tramitar la obtención de un certificado de sello digital por cada uno de sus establecimientos. El Servicio de Administración Tributaria establecerá mediante reglas de carácter general los requisitos de control e identificación a que se sujetará el uso del sello digital de los contribuyentes.

La tramitación de un certificado de sello digital sólo podrá efectuarse mediante formato electrónico que cuente con la firma electrónica avanzada de la persona solicitante.

III. Cumplir los requisitos establecidos en el artículo 29-A de este Código.

IV. Remitir al Servicio de Administración Tributaria, antes de su expedición, el comprobante fiscal digital por Internet respectivo a través de los mecanismos digitales que para tal efecto determine dicho órgano desconcentrado mediante reglas de carácter general, con el objeto de que éste proceda a:

a) Validar el cumplimiento de los requisitos establecidos en el artículo 29-A de este Código.

b) Asignar el folio del comprobante fiscal digital.

c) Incorporar el sello digital del Servicio de Administración Tributaria.

El Servicio de Administración Tributaria podrá autorizar a proveedores de certificación de comprobantes fiscales digitales por Internet para que efectúen la validación, asignación de folio e incorporación del sello a que se refiere esta fracción.

Los proveedores de certificación de comprobantes fiscales digitales por Internet a que se refiere el párrafo anterior deberán estar previamente autorizados por el Servicio de Administración Tributaria y cumplir con los requisitos que al efecto establezca dicho órgano desconcentrado mediante reglas de carácter general.

El Servicio de Administración Tributaria podrá revocar las autorizaciones emitidas a los proveedores a que se refiere esta fracción, cuando incumplan con alguna de las obligaciones establecidas en este artículo, en la autorización respectiva o en las reglas de carácter general que les sean aplicables.

Para los efectos del segundo párrafo de esta fracción, el Servicio de Administración Tributaria podrá proporcionar la información necesaria a los proveedores autorizados de certificación de comprobantes fiscales digitales por Internet.

V. Una vez que se incorpore el sello digital del Servicio de Administración Tributaria al comprobante fiscal digital por Internet, deberán entregar o poner a disposición de sus clientes, a través de los medios electrónicos que disponga el citado órgano desconcentrado mediante reglas de carácter general, el archivo electrónico del comprobante fiscal digital por Internet de que se trate y, cuando les sea solicitada por el cliente, su representación impresa, la cual únicamente presume la existencia de dicho comprobante fiscal.

VI. Cumplir con las especificaciones que en materia de informática determine el Servicio de Administración Tributaria mediante reglas de carácter general.

Los contribuyentes podrán comprobar la autenticidad de los comprobantes fiscales digitales por Internet que reciban consultando en la página de Internet del Servicio de Administración Tributaria si el número de folio que ampara el comprobante fiscal digital fue autorizado al emisor y si al momento de la emisión del comprobante fiscal digital, el certificado que ampare el sello digital se encontraba vigente y registrado en dicho órgano desconcentrado.

En el caso de las devoluciones, descuentos y bonificaciones a que se refiere el artículo 25 de la Ley del Impuesto sobre la Renta, se deberán expedir comprobantes fiscales digitales por Internet.

El Servicio de Administración Tributaria, mediante reglas de carácter general, podrá establecer facilidades administrativas para que los contribuyentes emitan sus comprobantes fiscales digitales por medios propios, a través de proveedores de servicios o con los medios electrónicos que en dichas reglas determine. De igual forma, a través de las citadas reglas podrá establecer las características de los comprobantes que servirán para amparar el transporte de mercancías, así como de los comprobantes que amparen operaciones realizadas con el público en general.

Tratándose de actos o actividades que tengan efectos fiscales en los que no haya obligación de emitir comprobante fiscal digital por Internet, el Servicio de Administración Tributaria podrá, mediante reglas de carácter general, establecer las características de los documentos digitales que amparen dichas operaciones.

Artículo 29-A. Los comprobantes fiscales digitales a que se refiere el artículo 29 de este Código deberán contener los siguientes requisitos:

I. La clave del registro federal de contribuyentes de quien los expida y el régimen fiscal en que tributen conforme a la Ley del Impuesto sobre la Renta. Tratándose de contribuyentes que tengan más de un local o establecimiento, se deberá señalar el domicilio del local o establecimiento en el que se expidan los comprobantes fiscales.

II. El número de folio y el sello digital del Servicio de Administración Tributaria, referidos en la fracción IV, incisos b) y c) del artículo 29 de este Código, así como el sello digital del contribuyente que lo expide.

III. El lugar y fecha de expedición.

IV. La clave del registro federal de contribuyentes de la persona a favor de quien se expida. Cuando no se cuente con la clave del registro federal de contribuyentes a que se refiere esta fracción, se señalará la clave genérica que establezca el Servicio de Administración Tributaria mediante reglas de carácter general, considerándose la operación como celebrada con el público en general.

V. La cantidad, unidad de medida y clase de los bienes o mercancías o descripción del servicio o del uso o goce que amparen, estos datos se asentarán en los comprobantes fiscales digitales por Internet usando los catálogos incluidos en las especificaciones tecnológicas a que se refiere la fracción VI del artículo 29 de este Código.

VI. El valor unitario consignado en número.

VII. El importe total consignado en número o letra, conforme a lo siguiente:

a) Cuando la contraprestación se pague en una sola exhibición, en el momento en que se expida el comprobante fiscal digital por Internet correspondiente a la operación de que se trate, se señalará expresamente dicha situación, además se indicará el importe total de la operación y, cuando así proceda, el monto de los impuestos trasladados desglosados con cada una de las tasas del impuesto correspondiente y, en su caso, el monto de los impuestos retenidos.

b) Cuando la contraprestación no se pague en una sola exhibición, o pagándose en una sola exhibición, ésta se realice de manera diferida del momento en que se emite el comprobante fiscal digital por Internet que ampara el valor total de la operación, se emitirá un comprobante fiscal digital por Internet por el valor total de la operación en el momento en que ésta se realice y se expedirá un comprobante fiscal digital por Internet por cada uno del resto de los pagos que se reciban.

c) Señalar la forma en que se realizó el pago, ya sea en efectivo, transferencias electrónicas de fondos, cheques nominativos o tarjetas de débito, de crédito, de servicio o las denominadas monederos electrónicos que autorice el Servicio de Administración Tributaria.

VIII. Tratándose de mercancías de importación:

a) El número y fecha del documento aduanero, tratándose de ventas de primera mano.

b) En importaciones efectuadas a favor de un tercero, el número y fecha del documento aduanero, los conceptos y montos pagados por el contribuyente directamente al proveedor extranjero y los importes de las contribuciones pagadas con motivo de la importación.

IX. Los contenidos en las disposiciones fiscales, que sean requeridos y dé a conocer el Servicio de Administración Tributaria, mediante reglas de carácter general.

De manera adicional, se debe revisar el anexo 20 del SAT que contiene la guía de llenado del CFDI para revisar de manera específica el llenado de los CFDIS versión 3.3

B. Resolución Miscelánea Fiscal para 2021

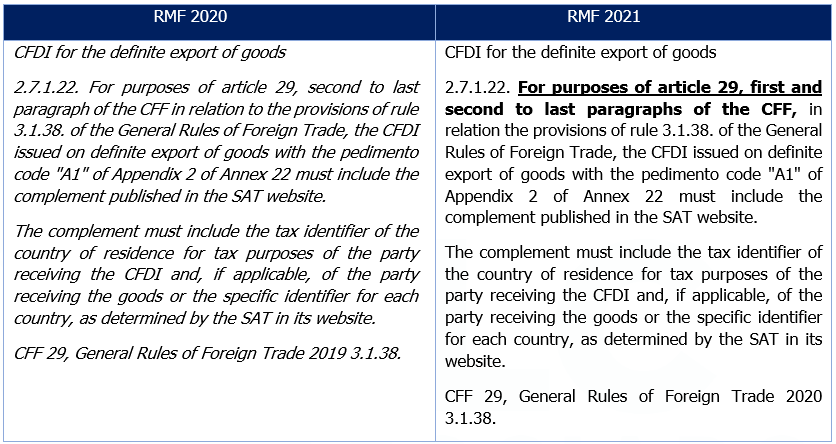

Complemento de CFDI en exportación definitiva de mercancías

2.7.1.22. Para los efectos del artículo 29, primer y penúltimo párrafos del CFF en relación con lo dispuesto por la regla 3.1.38. de las Reglas Generales de Comercio Exterior, al CFDI que se emita con motivo de operaciones de exportación definitiva de mercancías con clave de pedimento “A1” del Apéndice 2 del Anexo 22 de las citadas Reglas Generales, deberá incorporársele el Complemento que al efecto se publique en el Portal del SAT.

En el citado Complemento se deberá incluir el identificador fiscal del país de residencia para efectos fiscales del receptor del CFDI y, en su caso, del destinatario de la mercancía, o el identificador específico para cada país, que al efecto determine el SAT en su Portal.

CFF 29, Reglas Generales de Comercio Exterior 2020 3.1.38.

C. Reglas Generales de Comercio Exterior para 2020

Transmisión de información contenida en el CFDI

3.1.38. Para los efectos de los artículos 36 y 36-A, fracción II, inciso a) de la Ley, quienes exporten mercancías de manera definitiva con la clave de pedimento “A1” del Apéndice 2 del Anexo 22 y las mismas sean objeto de enajenación en términos del artículo 14 del CFF, deberán transmitir el archivo electrónico del CFDI y asentar en el campo correspondiente del pedimento, los números de folios fiscales de los CFDI.

En el CFDI emitido conforme a los artículos 29 y 29-A del CFF a que se refiere la presente regla, se deberán incorporar los datos contenidos en el complemento que al efecto publique el SAT en su Portal, en términos de la regla 2.7.1.22., de la RMF.

En los casos en los que, en términos de la presente regla, se transmita el CFDI con los datos referidos en el párrafo anterior, excepto tratándose de pedimentos consolidados a que se refiere la regla 1.9.19., no será necesario efectuar la transmisión del acuse de valor previsto en la regla 1.9.18.

Ley 36, 36-A-II, 59-A, 89, 102, CFF 14, 17-D, 17-E, 17-F, 17-G, 29, 29-A, RGCE 1.9.18., 1.9.19. Anexo 22, RMF 2.7.1.22.

“En TLC Asociados, desarrollamos un equipo multidisciplinario de expertos en auditorías y análisis de riesgos para asesorar y dar cumplimiento en operaciones de comercio exterior”.

Para más información o comentarios sobre esta publicación contacte a:

TLC Asociados, S. C.

Prohibida la reproducción parcial o total. Todos los derechos reservados de TLC Asociados, S. C. El contenido del presente articulo no constituye una consulta particular y por lo tanto TLC Asociados, S. C., su equipo y su autor, no asumen responsabilidad alguna de la interpretación o aplicación que el lector o destinatario le pueda dar.

I. Approach

“Export operations with A1 pedimento code, including those carried out by IMMEX companies in which, in accordance with Article 29 of the Federal Fiscal Code, the digital tax receipt (CFDI for its Spanish acronym) must be declared”.

II. Comment

1. Derived from the Reform of Article 29 of the Federal Fiscal Code (hereinafter CFF) published in the DOF on December 8, 2020, as of January 1, 2021 it is mandatory to issue a CFDI of Transfer in definitive export operations with pedimento code A1 in those cases where the goods are not subject to disposal or are free of charge.

Article 29 of the CFF establishes the obligation to issue the CFDI for different activities, as well as article 29-A of the CFF establishes the general requirements to be complied in any CFDI. Also, in this specific case, it will be necessary to follow the Annex 20 guide issued by the SAT as well as the guide for filling out the voucher that incorporates the complement for foreign trade to see the specifications for filling out the CFDI.

With regard to the amendment to the Federal Fiscal Code, an amendment related to the Digital Tax Receipt by Internet and the export operations of goods that are not subject to sale or when the sale is free of charge was announced, which to the letter, states the following:

“Article 29. When the tax laws establish the obligation to issue tax receipts for their carried out activities, the income received, or their withholdings, the taxpayer mut issue them digitaly using the website of the Tax Administration Service. Those who acquire goods, enjoy their temporary use or possession, receive services, make partial or deferred payments that settle balances of digital tax receipts through the Internet, export goods that are not sold or whose sale is free of charge, or those from whom taxes have been withheld, must request the respective digital tax receipt through the Internet.

2. The update of the new rule 2.7.1.22 of the RMF 2021 in relation to the RMF 2020, only incorporates the grounds of the first paragraph of Article 29 of the CFF that refers to the issuance of a CFDI of Transfer in definitive export operations with customs declaration code A1 in cases where the goods are not subject to sale or are free of charge, which corresponds to the reform of the CFF on December 8, 2020.

3. The obligation to issue the CFDI of transfer for definite exports for tax purposes is found in rule 2.7.1.22 of the RMF 2021 and, in matters of foreign trade, in rule 3.1.38 of the RGCE for 2020.

In general terms, rule 2.7.1.22 does not mention that the obligation is exclusive for the “alienation of goods in terms of article 14 of the CFF” as stated in rule 3.1.38 of the RGCE for 2020. Therefore, it can be understood that it is applicable to diferent alienation situations, such is the case of the goods that are not subject to alienation or are free of charge.

In this sense, derived from the amendment to article 29 of the CFF and rule 2.7.1.22 RMF 2021, the assumption of issuing a CFDI for goods that are not subject to alienation or are free of charge is also contemplated.

It is worth mentioning that rule 3.1.38 of the RGCE 2020 has not yet been amended to establish the strict obligation in foreign trade operations.

4. In terms of foreign trade, it is possible to issue the CFDI of Transfer in export operations with the pedimento code “A1” in those cases in which the goods are not subject to alienation or are free of charge.

The “Guideline for filling out the invoice to which the complement for foreign trade is incorporated” issued in the 2020 period mentions the following:

A. Free disposal

In the case of definitive exports with pedimento code “A1” in which the goods are sold, but such sale is made free of charge, the taxpayer may choose to use any of the following mechanisms, always with version 1.1 of the foreign trade complement:

a) Issue the receipt as type “I” (Income) in which the description and the mercantile value of the goods are included and then establish a discount for the same amount of these, so that the CFDI results with value “0”, in addition to incorporating the complement, without including the “Owner” node and the “Reason for Transfer” field.

b) Issue the receipt as type “T” (Transfer), and incorporate the complement that includes the “Owner” node and the “Reason for Transfer” field.

B) There is no alienation

However, in the case of definitive exports of goods with pedimento code “A1”, when there is no alienation of such goods in terms of article 14 of the CFF, it is not mandatory to use the complement for foreign trade. Taxpayers who voluntarily wish to do so may issue the CFDI in accordance with item b) described in this section. In these cases, however, it is necessary to continue to include the acknowledgement of value and declare in the corresponding pedimento, in field “505”, the tax folio number of the CFDI, as well as the acknowledgement of value referred to in rule 1.9.18. of the RGCE in force.

http://omawww.sat.gob.mx/tramitesyservicios/Paginas/documentos/GuiaComercioExterior3_3.pdf

However, in the future, the tax authority should update this manual of guidelines to specify in a new filling guide, whether the CFDI transfer requires the Foreign Trade Complement or whether it will continue to be optional.

5. The Customs Broker or Customs Agency has no obligation to verify the folio of the CFDI Transfer.

In terms of rule 3.1.39 of the RGCE for 2020, it is mentioned that, in relation to rule 3.1.38 of the aforementioned provision, customs agents, customs agencies or customs agents must verify that the tax folio number or numbers of the CFDI correspond to the one that appears in the SAT Portal when acting on their behalf, when determining the applicable taxes. Therefore, there is no obligation to verify the number or fiscal folio number of the CFDI Transfer.

6. The Customs Broker or Customs Agency has no obligation to digitize the CFDI and the content of the XML file.

Fact sheet 17 dated June 30, 2016 mentions that in transactions carried out under rule 3.1.35 RGCE 2016, with the exception of the second paragraph (currently 3.1.38 RGCE 2020), they must transmit the CFDI and XML (whether or not it has a complement) as a digital document at the Single Window, with the label 170 (Invoice or CFDI).

Therefore, it would not be applicable to the CFDI Transfer procedure established in Article 29 CFF and described in rule 2.7.1.22 of the RMF for 2020.

https://www.ventanillaunica.gob.mx/vucem/meses/junio2016/hojainfo17.pdf

7. Filling out the Transfer CFDI

The transfer CFDI must comply with all the general requirements of Article 29-A of the Tax Code. Furthermore, in accordance with the guidelines for filling out Annex 20 issued by the SAT and the Guide for filling out the invoice that incorporates the complement for foreign trade applicable to version 3.3 of the CFDI and the complement for foreign trade version 1.1, it must contain at least the following:

- It must be indicated that it is a transfer CFDI (T)

- RFC of the issuer

- RFC of the recipient

- Tax folio number

- Tax Address

- Concept according to the SAT catalog

- Amount according to the SAT catalog

- Units of measure according to SAT catalog

- Corresponding XML

- Digital seal

- QR Code

- Unit value must be zero

- Subtotal and total must be zero

According to the filling guide of annex 20, in the concept of the information, it is necessary to fill out in detail what the goods being transported consist of.

The type of receipt registered is “T” (Transfer) and the following points should be considered:

- The Transfer Reason field must be recorded

- If Code 05 (shipment of goods owned by third parties) is entered in the reason for shipment field, at least one owner must be entered.

- If the codes 01 (shipment of previously invoiced goods), 02 (relocation of own goods), 03 (shipment of goods subject to consignment contract) or 04 (shipment of goods for subsequent disposal) are entered, the owner node must NOT be entered.

In this type of receipt, the following fields should not exist:

- Payment terms

- Discount of the concepts

- The Payment Method Tax node

- Payment Method

- Discount field

- Withholdings

The CFDI does not replace the need to include the necessary documentation for the legal stay of the goods. It is suggested to review the filling guide annex 20 and the foreign trade guide for its correct application.

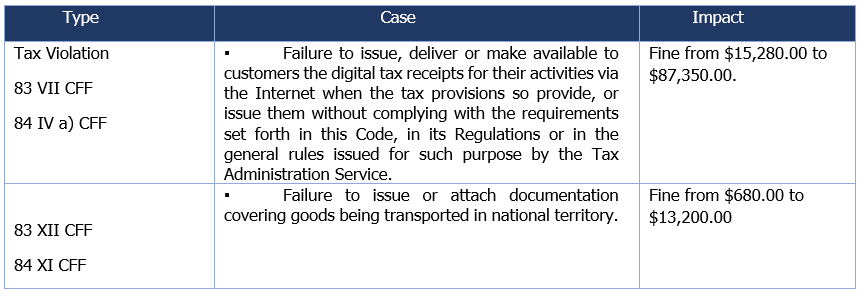

8. The tax risks for the IMMEX company for not issuing the Transfer CFDI are the infractions and sanctions that are indicated:

III. Grounds

A. Federal Fiscal Code

Article 14. Alienation of assets is understood to be:

I. Any change of ownership, even if the disposing party reserves the ownership of the transferred property.

II. The adjudications, even when made in favor of the creditor.

III. Contribution to a company or association.

IV. Those carried out by means of financial leasing.

V. Those carried out through the trusteeship, in the following cases:

a) In the act in which the settlor designates or undertakes to designate a trustee other than himself, provided that he is not entitled to reacquire the assets from the trustee.

b) In the act in which the settlor loses the right to reacquire the assets of the trustee, if such right had been reserved.

When the settlor receives certificates of participation for the assets it assigns in trust, such assets will be considered disposed of at the time the settlor receives the certificates, except in the case of shares.

VI. The assignment of the rights held over the assets subject to the trust, at any of the following times:

a) Upon the act in which the appointed trustee assigns his rights or gives instructions to the trustee to transfer the ownership of the assets to a third party. In these cases, the trustee shall be deemed to acquire the assets in the act of his appointment and to dispose of them at the time of assigning his rights or giving such instructions.

b) In the act in which the settlor assigns his rights if these include the right to have the assets transferred in his favor.

When certificates of participation are issued for the assets subject to the trust and are placed among the general investing public, such assets will not be considered disposed of when such certificates are disposed of, unless they give their holders direct rights of use of such assets, or if they are shares. The alienation of the certificates of participation will be considered as an alienation of debt securities that do not represent the ownership of assets and will have the tax consequences established by the tax laws for the alienation of such securities.

VII. The transfer of ownership of tangible property or of the right to acquire it through the sale of debt instruments or the assignment of rights representing them.

The provisions of this section are not applicable to shares or partnership interests.

VIII. The transfer of credit rights related to the supply of goods, services or both through a financial factoring contract at the time of the execution of such contract, except when they are transferred through factoring with collection mandate or delegated collection, as well as in the case of transfer of credit rights in charge of individuals, in which case it will be considered that there is a transfer until the corresponding credits are collected.

The one carried out by means of corporate mergers or spin-offs, except in the cases referred to in Article 14-B of this Code.

It is understood that sales are made with deferred payment or in installments when they are made with customers who are the general public, when more than 35% of the price is deferred until after the sixth month and when the agreed term exceeds twelve months. Transactions carried out with the general public are considered as such when the simplified tax receipts referred to in this Code are issued for such transactions.

It is considered that the alienation is carried out in national territory, among other cases, if the good is in such territory when the shipment is made to the acquirer and when not having shipment, in the country the material delivery of the good is carried out by the alienating party.

When in accordance with this Article it is understood that there is alienation, the acquirer will be considered owner of the goods for tax purposes.

“Article 29. When the tax laws establish the obligation to issue tax receipts for their carried out activities, the income received, or their withholdings, the taxpayer mut issue them digitaly using the website of the Tax Administration Service. Those who acquire goods, enjoy their temporary use or possession, receive services, make partial or deferred payments that settle balances of digital tax receipts through the Internet, export goods that are not sold or whose sale is free of charge, or those from whom taxes have been withheld, must request the respective digital tax receipt through the Internet.

The taxpayers mentioned in the previous paragraph must comply with the following obligations:

I. To have a valid advanced electronic signature certificate.

II. To obtain the certificate for the use of digital seals from the Tax Administration Service.

Taxpayers may decide to use one or more digital stamp certificates to be used exclusively for the issuance of tax receipts through digital documents. The digital seal will allow to certify the authorship of the digital tax receipts issued by individuals and legal entities through the Internet, which is subject to the regulations applicable to the use of the advanced electronic signature.

Taxpayers may obtain a digital seal certificate to be used by all their establishments or premises, or they may obtain a digital seal certificate for each of their establishments. The Tax Administration Service will establish by means of general rules the control and identification requirements to which the use of the digital seal of taxpayers will be subject.

The processing of a digital seal certificate may only be carried out by means of an electronic format with the advanced electronic signature of the applicant.

III. Comply with the requirements established in Article 29-A of this Code.

IV. Submit to the Tax Administration Service, prior to its issuance, the respective digital tax receipt by Internet through the digital mechanisms determined for such purpose by such decentralized agency by means of general rules, so that it may proceed to:

a) Validate compliance with the requirements established in Article 29-A of this Code.

b) Assign the folio number of the digital tax receipt.

c) Incorporate the digital seal of the Tax Administration Service.

The Tax Administration Service may authorize certification providers of digital tax receipts through the Internet to carry out the validation, folio assignment and incorporation of the seal referred to in this section.

The suppliers of certification of digital tax receipts by Internet referred to in the preceding paragraph must be previously authorized by the Tax Administration Service and comply with the requirements established by such decentralized body by means of general rules.

The Tax Administration Service may revoke the authorizations issued to the suppliers referred to in this section, when they fail to comply with any of the obligations established in this article, in the respective authorization or in the general rules applicable to them.

For the purposes of the second paragraph of this section, the Tax Administration Service may provide the necessary information to the authorized providers of certification of digital tax receipts through the Internet.

V. Once the digital seal of the Tax Administration Service is incorporated to the digital tax receipt by Internet, they must deliver or make available to their clients, through the electronic means provided by said decentralized body by means of general rules, the electronic file of the digital tax receipt by Internet in question and, when requested by the client, its printed representation, which only presumes the existence of said tax receipt.

VI. Comply with the IT specifications determined by the Tax Administration Service by means of general rules.

Taxpayers may verify the authenticity of the digital tax receipts received by Internet by consulting on the Tax Administration Service’s website whether the folio number that covers the digital tax receipt was authorized to the issuer and whether at the time the digital tax receipt was issued, the certificate that covers the digital seal was in force and registered in such decentralized agency.

In the case of refunds, discounts and bonuses referred to in Article 25 of the Income Tax Law, digital tax receipts must be issued via the Internet.

The Tax Administration Service, by means of general rules, may establish administrative facilities for taxpayers to issue their digital tax receipts by their own means, through service providers or with the electronic means determined in such rules. In addition, by means of the mentioned rules, it may establish the characteristics of the receipts that will be used to cover the transportation of goods, as well as the receipts that cover transactions carried out with the general public.

In the case of acts or activities that have tax effects in which there is no obligation to issue digital tax receipts through the Internet, the Tax Administration Service may, by means of general rules, establish the characteristics of the digital documents that cover such transactions.

Article 29-A. The digital tax receipts referred to in Article 29 of this Code must contain the following requirements:

I. The federal taxpayer registry number of the person issuing them and the tax regime under which they are taxed in accordance with the Income Tax Law. In the case of taxpayers who have more than one premises or establishment, the address of the premises or establishment where the tax receipts are issued must be indicated.

II. The folio number and the digital seal of the Tax Administration Service, referred to in section IV, paragraphs b) and c) of Article 29 of this Code, as well as the digital seal of the issuing taxpayer.

III. Place and date of issue

IV. The federal taxpayer registry number of the person in favor of whom it is issued. When the taxpayers’ federal registry code referred to in this section is not available, the generic code established by the Tax Administration Service by means of general rules will be used, and the transaction will be considered as one entered into with the general public.

V. The amount, unit of measurement and class of the goods or merchandise or description of the service or use or enjoyment that they cover, this data will be recorded in the digital tax receipts by Internet using the catalogs included in the technological specifications referred to in section VI of article 29 of this Code.

VI. The unit value entered in number.

VII. The total amount stated in number or letter, in accordance with the following:

a) When the consideration is paid in a single installment, at the time the digital tax receipt is issued through the Internet corresponding to the transaction in question, this situation will be expressly indicated, in addition to the total amount of the transaction and, when applicable, the amount of the taxes transferred broken down with each of the corresponding tax rates and, if applicable, the amount of the taxes withheld.

b) When the consideration is not paid in a single installment, or if it is paid in a single installment, the payment is deferred from the moment in which the digital tax receipt is issued for the total value of the transaction, a digital tax receipt will be issued for the total value of the transaction at the moment in which the transaction is made and a digital tax receipt will be issued for each of the rest of the payments received.

c) Indicate the form in which the payment was made, whether in cash, electronic fund transfers, nominative checks or debit, credit or service cards or the so-called electronic purses authorized by the Tax Administration Service.

VIII. In the case of imported goods:

a) The number and date of the customs document, in the case of first-hand sales.

b) In imports made in favor of a third party, the number and date of the customs document, the items and amounts paid by the taxpayer directly to the foreign supplier and the amounts of taxes paid on the import.

Those included in the tax provisions, which are required and disclosed by the Tax Administration Service, through general rules.

In addition, Annex 20 of the SAT, which contains the CFDI filling guide, should be reviewed to specifically review the filling of CFDIS version 3.3.

B) Miscellaneous Tax Resolution for 2021

CFDI for the definite export of goods

2.7.1.22. For purposes of article 29, first and second to last paragraphs of the CFF, in relation the provisions of rule 3.1.38. of the General Rules of Foreign Trade, the CFDI issued on definite export of goods with the pedimento code “A1” of Appendix 2 of Annex 22 must include the complement published in the SAT website.

The complement must include the tax identifier of the country of residence for tax purposes of the party receiving the CFDI and, if applicable, of the party receiving the goods or the specific identifier for each country, as determined by the SAT in its website.

CFF 29, General Rules of Foreign Trade 2020 3.1.38.

C) General Rules of Foreign Trade for 2020

Disclosure of information contained in the CFDI

3.1.38. For purposes of articles 36 and 36-A, section II, subsection a) of the Law, those who export goods definitively using the pedimento code “A1” of Appendix 2 of Annex 22 and the goods are subject to alienation in terms of article 14 of the CFF must send the electronic file CFDI and fill in the fiscal folio numbers of the CFDI in the corresponding area of the pedimento.

In the CFDI issued according to Articles 29 and 29-A of the CFF referred to in this rule, the data specified in the complement published by the SAT on its website, in terms of rule 2.7.1.22 of the RMF, must be included.

In cases where, in terms of this rule, the CFDI is issued with the data referred to in the previous paragraph, except for consolidated pedimentos referred to by rule 1.9.19, it will not be necessary to issue the acknowledgment of value of rule 1.9.18.

Law 36, 36-A-II, 59-A, 89, 102, CFF 14, 17-D, 17-E, 17-F, 17-G, 29, 29-A, RGCE 1.9.18., 1.9.19. 19. Annex 22, RMF 2.7.1.22.

“In TLC Asociados, we develop a multidisciplinary team of experts in audits and risk analysis for consulting and ensuring compliance with foreign trade operations”.

For further information or comments regarding this article, please contact:

TLC Asociados, S. C.