C28 – CONAMER: proyecto de reforma del anexo 2.4.1 de las NOM’S/ CONAMER: Project to Amend Annex 2.4.1 of the Official Mexican Standards (NOMs)

El 30 de julio de 2020 se dio a conocer en el portal de la Comisión Nacional de Mejora Regulatoria, por sus siglas CONAMER, el Proyecto del “Acuerdo que modifica al diverso por el que la Secretaría de Economía emite reglas y criterios de carácter general en materia de Comercio Exterior”, mismo que contiene cambios importantes sobre el Anexo 2.4.1 de las Normas Oficiales Mexicanas de etiquetado, entre los que destacan a continuación:

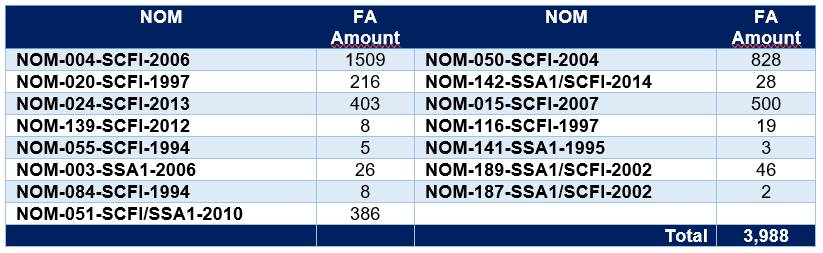

- El numeral 3 del Acuerdo del NOMs contiene 15 normas oficiales mexicanas relacionadas con la información comercial y sanitaria con un total aproximado de 3,988 fracciones arancelarias:

- Se modifica la fracción VIII relacionada con la nomenclatura NOM-051-SCFI/SSA1-2010 para indicar los requisitos del DOF del 5 de abril de 2010 y su modificación del 27 de marzo de 2020.

- Se reforma el numeral 6 para establecer el procedimiento del etiquetado de información comercial.

- En relación con el numeral 10 que contempla los supuestos de excepción del cumplimiento de NOM de seguridad, etiquetado de información comercial y las de emergencia, se realizan los siguientes cambios:

- Se deroga la fracción VII que considera excepciones del cumplimiento de NOMs cuando son utilizadas por personas físicas. Recordemos que, desde el 24 de octubre de 2018 y el 3 de junio de 2019, las NOMs de seguridad fueron obligatorias al momento de su importación a territorio nacional, salvo los regímenes aduaneros de diferimiento de arancel.

“VII. Las mercancías que se importen para ser usadas directamente por la persona física que las importe, para su uso directo, y que no se destinarán posteriormente a su comercialización directa o indirecta como parte de su actividad empresarial, siempre y cuando el importador, antes de activar el mecanismo de selección automatizado, anote en el pedimento de importación la clave que dé a conocer la SHCP para identificar las mercancías que se encuentren en los supuestos a que se refiere esta fracción.

Para tal efecto deberá anexar a dicho pedimento una declaración bajo protesta de decir verdad, indicando que las mercancías no se destinarán posteriormente a su comercialización directa o indirecta como parte de su actividad empresarial y señalar el lugar en el que usará dichas mercancías. Las mercancías correspondientes a la fracción arancelaria 9613.80.02 de la Tarifa y las mercancías clasificadas en las fracciones arancelarias sujetas al cumplimiento de las normas oficiales mexicanas NOM-218-SCFI- 2017, NOM-015-ENER-2012, NOM-208-SCFI-2016, NOM-026-ENER-2015, NOM-090- SCFI-2014, NOM-041-SEMARNAT-2015, NOM-192-SCFI/SCT1-2013, NOM-028-ENER- 2010, NOM-086-SCFI-2018, NOM-134-SCFI-1999, NOM-009-CONAGUA-2001, NOM-086/1-SCFI-2011, NOM-007-SCFI-2003, NOM-009-SCFI-1993, NOM-010-SESH-2012, NOM-011-ENER-2006, NOM-200-SCFI-2017, NOM-012-SCFI-1994, NOM-008- CONAGUA-1998, NOM-114-SCFI-2016, NOM-161-SCFI-2003, NOM-011-SCFI-2004, NOM-113-STPS-2009, NOM-001-ENER-2014, NOM-004-ENER-2014, NOM-005-ENER- 2016, NOM-006-CONAGUA-1997, NOM-005-SCFI-2017, NOM-010-SCFI-1994, NOM-013- SCFI-2004, NOM-014-SCFI-1997, NOM-016-ENER-2016, NOM-025-ENER-2013, NOM- 022-ENER/SCFI-2014, NOM-045-SCFI-2000, NOM-113-SCFI-1995, NOM-118-SCFI-2004, NOM-005-CONAGUA-1996, NOM-002-SEDE/ENER-2014, NOM-014-ENER-2004, NOM- 209-SCFI-2017, NOM-021-ENER/SCFI-2008, NOM-023-ENER-2018, NOM-031-ENER-2012, NOM-046-SCFI-1999, NOM-054-SCFI-1998, NOM-119-SCFI-2000, NOM-133/1- SCFI-1999, NOM-133/2-SCFI-1999, NOM-133/3-SCFI-1999, NOM-093-SCFI-1994, NOM- 063-SCFI-2001, NOM-001-SCFI-1993, NOM-003-SCFI-2014, NOM-010-CONAGUA-2000, NOM-016-SCFI-1993, NOM-017-ENER/SCFI-2012, NOM-019-SCFI-1998, NOM-030- ENER-2016, NOM-032-ENER-2013, NOM-058-SCFI-2017, NOM-064-SCFI-2000, NOM- 196-SCFI-2016, NOM-115-STPS-2009, NOM-121-SCFI-2004, NOM-220-SCFI-2017, NOM-008-SESH/SCFI-2010 y NOM-221-SCFI-2017, en ningún caso podrán acogerse a lo dispuesto en esta fracción;”

- Se deroga la fracción VIII que considera excepciones del cumplimiento de NOMs cuando son utilizadas por personas físicas o morales que son utilizadas para prestar los servicios profesionales, cuando son sometidas a procesos productivos o de empaque, o bien, tratándose de ventas entre empresas especializadas.

De igual manera, que el punto anterior desde el 24 de octubre de 2018 y el 3 de junio de 2019 la NOMs de seguridad fueron obligatorias al momento de su importación a territorio nacional, salvo los regímenes aduaneros de diferimiento de arancel.

“VIII. Las mercancías que no vayan a expenderse al público tal y como son importadas, siempre que el importador:

a) Las utilice en la prestación de sus servicios profesionales (incluidos los servicios de reparación en talleres profesionales en general) y no las destine a uso del público, debiendo anexar al pedimento de importación una declaración bajo protesta de decir verdad, en la que indique que utilizará personalmente las mercancías importadas para la prestación de sus servicios profesionales, señalando en qué consisten éstos, y que no comercializará las mercancías importadas ni las destinará a uso del público;

b) Las utilice para llevar a cabo sus procesos productivos, incluso si se trata de refacciones para la maquinaria productiva que utilice en dichos procesos, o de materiales, partes y componentes que el mismo importador incorporará a un proceso industrial que modifique la naturaleza de dichos materiales, partes y componentes y los transforme en unas mercancías distintas, que sólo serán ofrecidas al público previo cumplimiento con la o las NOMs aplicables; debiendo anexar al pedimento de importación una declaración bajo protesta de decir verdad, en la que indique que utilizará las mercancías importadas como refacciones de la maquinaria que utiliza para llevar a cabo en sus procesos productivos, o como materiales, partes o componentes de un proceso productivo en virtud del cual se modificará la naturaleza de las mercancías importadas y las transformará en unas mercancías distintas que sólo serán ofrecidas al público previo cumplimiento con la o las NOMs aplicables;

c) Las vaya a enajenar a personas morales, que a su vez las destinarán para la prestación de sus servicios profesionales (incluidos los servicios de reparación en general) o para el desarrollo de sus procesos productivos y no a uso del público (“enajenación entre empresas en forma especializada”), debiendo anexar al pedimento de importación una declaración bajo protesta de decir verdad, en la que indique que destinará las mercancías importadas a la enajenación exclusiva entre empresas, toda vez que con anterioridad a la enajenación, la empresa adquirente fue debidamente informada por el importador de las características técnicas de las mercancías que adquiere, y que éstas no serán objeto de reventa posterior al público en general, o

d) Las importe para destinarlas a procesos de acondicionamiento, envase y empaque final, en el caso de mercancías sujetas a NOMs de información comercial que se presenten al despacho aduanero en embalajes o empaques que, aun cuando ostenten marcas u otras leyendas, o señalen el contenido o cantidad, pueda demostrarse que están concebidos exclusivamente para contener y proteger dichas mercancías para efectos del transporte y almacenamiento antes de su acondicionamiento, envase y empaque en la forma final en la cual serán ofrecidas al público, debiendo anexar al pedimento de importación una declaración bajo protesta de decir verdad, en la que indique que acondicionará o envasara y empacará las mercancías importadas en los envases finales destinados a cumplir con las NOMs de información comercial correspondientes, antes de ser ofrecidas al público.

Para que proceda lo dispuesto en los incisos a) al d) anteriores, el importador deberá anotar en el pedimento de importación, antes de activar el mecanismo de selección automatizado, la clave que dé a conocer la SHCP para identificar las mercancías que se encuentren en los supuestos a que se refiere esta fracción. En la declaración bajo protesta de decir verdad, el importador deberá señalar adicionalmente el domicilio en el que destinará a uso propio, prestará sus servicios profesionales, utilizará o transformará conforme a su proceso productivo las mercancías importadas, se efectuará el servicio o proceso productivo de las mercancías importadas para enajenación en forma especializada, o se acondicionarán, envasarán y empacarán las mercancías en los envases finales que cumplirán con las NOM’s de información comercial correspondientes antes de ser ofrecidas al público, o aquel en el que mantendrá depositadas las mercancías importadas previo a la prestación de sus servicios, la utilización, transformación o reacondicionamiento. Las mercancías correspondientes a las fracciones arancelarias 2203.00.01, 3922.90.99, 6910.10.01, 6910.90.01 y 9613.80.02 de la Tarifa y las mercancías clasificadas en las fracciones arancelarias sujetas al cumplimiento de las normas oficiales mexicanas NOM-009-CONAGUA-2001, NOM-015-ENER-2012, NOM- 218-SCFI-2017, NOM-208-SCFI-2016, NOM-026-ENER-2015, NOM-090-SCFI-2014, NOM-041-SEMARNAT-2015, NOM-192-SCFI/SCT1-2013, NOM-028-ENER-2010, NOM- 086-SCFI-2018, NOM-134-SCFI-1999, NOM-086/1-SCFI-2011, NOM-007-SCFI-2003, NOM-009-SCFI-1993, NOM-010-SESH-2012, NOM-011-ENER-2006, NOM-200-SCFI- 2017, NOM-012-SCFI-1994, NOM-008-CONAGUA-1998, NOM-114-SCFI-2016, NOM-161- SCFI-2003, NOM-011-SCFI-2004, NOM-113-STPS-2009, NOM-001-ENER-2014, NOM- 004-ENER-2014, NOM-005-ENER-2016, NOM-006-CONAGUA-1997, NOM-005-SCFI-2017, NOM-010-SCFI-1994, NOM-013-SCFI-2004, NOM-014-SCFI-1997, NOM-016- ENER-2016, NOM-025-ENER-2013, NOM-022-ENER/SCFI-2014, NOM-045-SCFI-2000, NOM-113-SCFI-1995, NOM-118-SCFI-2004, NOM-005-CONAGUA-1996, NOM-002- SEDE/ENER-2014, NOM-014-ENER-2004, NOM-209-SCFI-2017, NOM-021-ENER/SCFI- 2017, NOM-023-ENER-2018, NOM-031-ENER-2012, NOM-046-SCFI-1999, NOM-054- SCFI-1998, NOM-119-SCFI-2000, NOM-133/1-SCFI-1999, NOM-133/2-SCFI-1999, NOM- 133/3-SCFI-1999, NOM-093-SCFI-1994, NOM-063-SCFI-2001, NOM-001-SCFI-1993, NOM-003-SCFI-2014, NOM-010-CONAGUA-2000, NOM-016-SCFI-1993, NOM-017- ENER/SCFI-2012, NOM-019-SCFI-1998, NOM-030-ENER-2016, NOM-032-ENER-2013, NOM-058-SCFI-2017, NOM-064-SCFI-2000, NOM-196-SCFI-2016, NOM-115-STPS-2009, NOM-121-SCFI-2004, NOM-220-SCFI-2017, NOM-008-SESH/SCFI-2010 y NOM-221-SCFI-2017, no podrán acogerse a lo dispuesto en esta fracción en ningún caso.

Para los efectos del párrafo anterior, tratándose de empresas con Programa IMMEX autorizado por la SE, no será necesario que anexen al pedimento de importación la declaración bajo protesta de decir verdad a que se refiere el párrafo anterior.”

- Se deroga la fracción XV que es utilizada por los importadores con registro de empresas de la región o franja fronteriza emitido por la Secretaría de Economía.

XV. Tratándose de las NOMs NOM-004-SCFI-2006, NOM-015-SCFI-2007, NOM-020-SCFI- 1997, NOM-024-SCFI-2013, NOM-050-SCFI-2004, NOM-051-SCFI/SSA1-2010, NOM-186- SSA1/SCFI-2013, NOM-189-SSA1/SCFI-2002 y NOM-141-SSA1/SCFI-2012, las mercancías destinadas a permanecer en las franjas y regiones fronterizas del país importadas por personas físicas o morales ubicadas en dichas franjas y regiones fronterizas que realicen actividades de comercialización, presten servicios de restaurantes, hoteles, esparcimiento, culturales, recreativos, deportivos, educativos, investigación, médicos y de asistencia social; alquiler de bienes muebles y servicios prestados a las empresas, según la clasificación del Catálogo de Actividades Económicas que da a conocer el SAT mediante reglas de carácter general y que cuenten con registro como empresas de la frontera en términos del Decreto por el que se establece el impuesto general de importación para la región fronteriza y la franja fronteriza norte.

Para los efectos de esta fracción, se consideran como franjas y regiones fronterizas a la franja Norte colindante con los Estados Unidos de América, la franja fronteriza Sur colindante con Guatemala, los estados de Baja California, Baja California Sur y Quintana Roo, la región parcial de Sonora, y los municipios de Caborca, Sonora, Cananea, Sonora, Salina Cruz, Oaxaca, Comitán de Domínguez, Chiapas y Tenosique, Tabasco.

La franja fronteriza Norte colindante con los Estados Unidos de América está conformada por el territorio comprendido entre la línea divisoria internacional del Norte del país y la línea paralela a una distancia de 20 kilómetros hacia el interior del país, en el tramo comprendido entre el límite de la región parcial del Estado de Sonora y el Golfo de México, así como el Municipio Fronterizo de Cananea, Sonora.

La franja fronteriza Sur colindante con Guatemala, es la zona comprendida por el territorio de 20 kilómetros paralelo a la línea divisoria internacional del Sur del país, en el tramo comprendido entre el Municipio Unión Juárez y la desembocadura del Río Suchiate en el Océano Pacífico, dentro del cual se encuentra el municipio de Tapachula, Chiapas, con los límites que geográficamente le corresponden.

La región parcial del Estado de Sonora es la comprendida en los siguientes límites: al norte, la línea divisoria internacional desde el cauce actual del Río Colorado hasta el punto situado en esa línea a 10 kilómetros al Oeste de Sonoyta, de ese punto, una línea recta hasta llegar a la costa, a un punto situado a 10 kilómetros al este de Puerto Peñasco; de allí, siguiendo el cauce de ese río, hacia el norte hasta encontrar la línea divisoria internacional.

Para que proceda lo dispuesto en esta fracción serán requisitos:

a) Que el importador anote en el pedimento de importación, antes de activar el mecanismo de selección automatizado, la clave que dé a conocer la SHCP para identificar las mercancías que se encuentren en los supuestos de esta fracción, y

b) Que el importador presente declaración bajo protesta de decir verdad, indicando que las mercancías cumplirán con los requisitos de información comercial establecidos en las NOMs NOM-004-SCFI-2006, NOM-015-SCFI-2007, NOM-020-SCFI-1997, NOM- 024-SCFI-2013, NOM-050-SCFI-2004, NOM-051-SCFI/SSA1-2010, NOM-186- SSA1/SCFI-2013, NOM-189-SSA1/SCFI-2002 y NOM-141-SSA1/SCFI-2012 en los términos del procedimiento simplificado que al efecto expida la SE, por conducto de la Dirección General de Normas, y que no las reexpedirá al resto del país, salvo en los términos y disposiciones que se establezcan en dicho procedimiento y en la legislación aduanera.

Las mercancías correspondientes a las fracciones arancelarias 1601.00.01, 1601.00.99, 1602.31.01, 1602.32.01, 1602.41.01, 1602.42.01, 1602.50.99, 1902.11.01, 1902.19.99,1902.20.01, 1902.30.99, 1905.31.01, 1905.32.01 y 9619.00.01 de la Tarifa en ningún caso podrán acogerse a lo dispuesto en esta fracción.

- Es importante revisar las alternativas para la importación definitiva de mercancías que se someterán a procesos productivos sobre todo aquellas que cuentan con la autorización de algún sector de los Programas de Promoción Sectorial.

- La reforma del Anexo 2.4.1 tiene como fecha tentativa de entrar en vigor el 1 de octubre de 2020.

No obstante, existen algunas excepciones para el cumplimiento de los requisitos previstos para la NOM-051-SCFI/SSA1-2010 que tendrá vigencia el 1 de abril de 2021.

Por lo anterior, es recomendable que los actores del comercio exterior realicen planteamientos ante la CONAMER en el supuesto que consideren que pueden tener un impacto en los trámites de importación de sus mercancías. Liga: http://187.191.71.192/portales/resumen/49820

“En TLC Asociados desarrollamos un equipo multidisciplinario de expertos en auditorías y análisis de riesgos para asesorar, implementar estrategias y dar cumplimiento en operaciones de comercio exterior”.

Para más información o comentarios sobre esta publicación contacte a:

División de Consultoría

TLC Asociados SC

Prohibida la reproducción parcial o total. Todos los derechos reservados de TLC Asociados, S.C. El contenido del presente artículo no constituye una consulta particular y por lo tanto TLC Asociados, S.C., su equipo y su autor, no asumen responsabilidad alguna de la interpretación o aplicación que el lector o destinatario le pueda dar.

On July 30, 2020, the National Commission for Regulatory Improvement (CONAMER for its Spanish acronym) published a proposal for an “Agreement that modifies the various regulations by which the Secretariat of Economy issues general rules and criteria on foreign trade“, which contains important changes to Annex 2.4.1 of the Official Mexican Standards (NOM for its Spanish acronym) for Labeling, which include the following:

- Paragraph 3 of the NOMs Agreement contains 15 official Mexican standards related to trade and health information with a total of approximately 3,988 tariff items

- Section VIII related to the NOM-051-SCFI/SSA1-2010 nomenclature is modified to indicate the requirements of the DOF of April 5, 2010 and its modification of March 27, 2020.

- Paragraph 6 is amended to establish the procedure for the labeling of commercial information.

- The following changes are made to numeral 10, which contemplates the cases of exceptions to compliance with safety NOMs, labeling of commercial information and emergency situations:

The section VII that considers exceptions from compliance with NOMs when they are used by natural persons is repealed. It should be recalled that, as of October 24, 2018 and June 3, 2019, security NOMs were mandatory at the time of importation into national territory, with the exception of tariff deferral customs regimes.

“VII. The goods that are imported to be used directly by the natural person that imports them, for their direct use, and that will not be destined later to their direct or indirect commercialization as part of their business activity, as long as the importer, before activating the automated selection mechanism, writes down in the import pedimento the key that the SHCP gives to identify the goods that are in the cases referred to in this fraction.

For that purpose, he shall attach to the said application a declaration under protest that the goods will not be subsequently marketed directly or indirectly as part of his business and shall indicate the place where he will use the goods. The goods corresponding to tariff item 9613.80.02 of the Tariff and the goods classified in the tariff items subject to compliance with the Official Mexican Standards NOM-218-SCFI- 2017, NOM-015-ENER-2012, NOM-208-SCFI-2016, NOM-026-ENER-2015, NOM-090- SCFI-2014, NOM-041-SEMARNAT-2015, NOM-192-SCFI/SCT1-2013, NOM-028-ENER- 2010, NOM-086-SCFI-2018, NOM-134-SCFI-1999, NOM-009-CONAGUA-2001, NOM-086/1-SCFI-2011, NOM-007-SCFI-2003, NOM-009-SCFI-1993, NOM-010-SESH-2012, NOM-011-ENER-2006, NOM-200-SCFI-2017, NOM-012-SCFI-1994, NOM-008- CONAGUA-1998, NOM-114-SCFI-2016, NOM-161-SCFI-2003, NOM-011-SCFI-2004, NOM-113-STPS-2009, NOM-001-ENER-2014, NOM-004-ENER-2014, NOM-005-ENER- 2016, NOM-006-CONAGUA-1997, NOM-005-SCFI-2017, NOM-010-SCFI-1994, NOM-013- SCFI-2004, NOM-014-SCFI-1997, NOM-016-ENER-2016, NOM-025-ENER-2013, NOM- 022-ENER/SCFI-2014, NOM-045-SCFI-2000, NOM-113-SCFI-1995, NOM-118-SCFI-2004, NOM-005-CONAGUA-1996, NOM-002-SEDE/ENER-2014, NOM-014-ENER-2004, NOM- 209-SCFI-2017, NOM-021-ENER/SCFI-2008, NOM-023-ENER-2018, NOM-031-ENER-2012, NOM-046-SCFI-1999, NOM-054-SCFI-1998, NOM-119-SCFI-2000, NOM-133/1- SCFI-1999, NOM-133/2-SCFI-1999, NOM-133/3-SCFI-1999, NOM-093-SCFI-1994, NOM- 063-SCFI-2001, NOM-001-SCFI-1993, NOM-003-SCFI-2014, NOM-010-CONAGUA-2000, NOM-016-SCFI-1993, NOM-017-ENER/SCFI-2012, NOM-019-SCFI-1998, NOM-030- ENER-2016, NOM-032-ENER-2013, NOM-058-SCFI-2017, NOM-064-SCFI-2000, NOM- 196-SCFI-2016, NOM-115-STPS-2009, NOM-121-SCFI-2004, NOM-220-SCFI-2017, NOM-008-SESH/SCFI-2010 and NOM-221-SCFI-2017, may not benefit from the provisions of this section under any circumstances;”

- Section VIII, which considers exceptions to compliance with NOMs when they are used by individuals or companies to provide professional services, when they are subject to production or packaging processes, or in the case of sales between specialized companies, is repealed.

Similarly, as the previous point, from October 24, 2018 and June 3, 2019, the security NOMs were mandatory at the time of importation into national territory, except for the customs regimes of tariff deferral.

“VIII. Goods that are not to be sold to the public as imported, provided that the importer:

a) Uses them to provide his professional services (including repair services in professional workshops in general) and does not use them for public purposes, and must attach to the import pedimento a declaration under protest that he will personally use the imported goods for the provision of his professional services, indicating what these services consist of, and that he will not market the imported goods or use them for public purposes;

b) Uses them to carry out his production processes, even if they are spare parts for the production machinery that he uses in those processes, or materials, parts and components that the same importer will incorporate in an industrial process that changes the nature of those materials, parts and components and transforms them into different goods, which will only be offered to the public after compliance with the applicable NOMs; having to attach to the import pedimento a declaration under protest of truth, in which it indicates that it will use the imported goods as spare parts of the machinery that it uses to carry out its productive processes, or as materials, parts or components of a productive process by virtue of which the nature of the imported goods will be modified and transformed into different goods that will only be offered to the public after compliance with the applicable NOMs;

c) Dispose of them to legal entities, which in turn will use them for the provision of their professional services (including repair services in general) or for the development of their production processes and not for public use (“disposal between enterprises in a specialized manner”), and a declaration under protest must be attached to the import petition, indicating that it will use the imported goods for the exclusive purpose of inter-company sale, since prior to the sale, the acquiring company was duly informed by the importer of the technical characteristics of the goods it is acquiring, and that the goods will not be subsequently resold to the general public, or

d) Imports in order to use them for conditioning, packing and final packaging processes, in the case of goods subject to commercial information standards that are presented for customs clearance in packages or packaging that, even if they bear trademarks or other legends, or indicate the content or quantity, can be shown to be designed exclusively to contain and protect such goods for the purposes of transport and storage before conditioning, packaging in the final form in which they will be offered to the public, having to attach to the import pedimento a declaration under protest of truth, in which it indicates that it will condition or package and pack the imported goods in the final containers intended to comply with the corresponding commercial information NOMs, before being offered to the public.

In order for the provisions of points (a) to (d) above to apply, the importer shall, before activating the automated selection mechanism, enter on the import pedimento the key provided by the SHCP to identify the goods in the cases referred to in this section. In the declaration under protest of truth, the importer must additionally indicate the domicile in which he will destine for his own use, will render his professional services, will use or transform according to his productive process the imported goods, will perform the service or productive process of the imported goods for disposal in a specialized way, o the goods will be conditioned, wrapped and packed in the final packaging that will comply with the corresponding commercial information NOMs before being offered to the public, or the one in which the imported goods will be kept prior to the provision of their services, use, transformation or reconditioning. The goods corresponding to tariff items 2203.00.01, 3922.90.99, 6910.10.01, 6910.90.01 and 9613.80.02 of the Tariff and the goods classified in the tariff items subject to compliance with the Official Mexican Standards NOM-009-CONAGUA-2001, NOM-015-ENER-2012, NOM- 218-SCFI-2017, NOM-208-SCFI-2016, NOM-026-ENER-2015, NOM-090-SCFI-2014, NOM-041-SEMARNAT-2015, NOM-192-SCFI/SCT1-2013, NOM-028-ENER-2010, NOM- 086-SCFI-2018, NOM-134-SCFI-1999, NOM-086/1-SCFI-2011, NOM-007-SCFI-2003, NOM-009-SCFI-1993, NOM-010-SESH-2012, NOM-011-ENER-2006, NOM-200-SCFI- 2017, NOM-012-SCFI-1994, NOM-008-CONAGUA-1998, NOM-114-SCFI-2016, NOM-161- SCFI-2003, NOM-011-SCFI-2004, NOM-113-STPS-2009, NOM-001-ENER-2014, NOM- 004-ENER-2014, NOM-005-ENER-2016, NOM-006-CONAGUA-1997, NOM-005-SCFI-2017, NOM-010-SCFI-1994, NOM-013-SCFI-2004, NOM-014-SCFI-1997, NOM-016- ENER-2016, NOM-025-ENER-2013, NOM-022-ENER/SCFI-2014, NOM-045-SCFI-2000, NOM-113-SCFI-1995, NOM-118-SCFI-2004, NOM-005-CONAGUA-1996, NOM-002- SEDE/ENER-2014, NOM-014-ENER-2004, NOM-209-SCFI-2017, NOM-021-ENER/SCFI- 2017, NOM-023-ENER-2018, NOM-031-ENER-2012, NOM-046-SCFI-1999, NOM-054- SCFI-1998, NOM-119-SCFI-2000, NOM-133/1-SCFI-1999, NOM-133/2-SCFI-1999, NOM- 133/3-SCFI-1999, NOM-093-SCFI-1994, NOM-063-SCFI-2001, NOM-001-SCFI-1993, NOM-003-SCFI-2014, NOM-010-CONAGUA-2000, NOM-016-SCFI-1993, NOM-017- ENER/SCFI-2012, NOM-019-SCFI-1998, NOM-030-ENER-2016, NOM-032-ENER-2013, NOM-058-SCFI-2017, NOM-064-SCFI-2000, NOM-196-SCFI-2016, NOM-115-STPS-2009, NOM-121-SCFI-2004, NOM-220-SCFI-2017, NOM-008-SESH/SCFI-2010 and NOM-221-SCFI-2017, may not benefit from the provisions of this section under any circumstances.

For the purposes of the previous paragraph, in the case of companies with an IMMEX Program authorized by the SE, it shall not be necessary to attach to the import request the declaration under protest referred to in the previous paragraph.”

- Section XV, which is used by importers with a business registration in the region or border area issued by the Secretariat of Economy, is repealed.

XV. For Standards NOM-004-SCFI-2006, NOM-015-SCFI-2007, NOM-020-SCFI- 1997, NOM-024-SCFI-2013, NOM-050-SCFI-2004, NOM-051-SCFI/SSA1-2010, NOM-186- SSA1/SCFI-2013, NOM-189-SSA1/SCFI-2002 y NOM-141-SSA1/SCFI-2012, the goods intended to remain in the border areas and regions of the country imported by natural or legal persons located in those border areas and regions who carry out marketing activities, provide restaurant, hotel, leisure, cultural, recreational, sporting, educational, research, medical and social assistance services; rental of movable goods and services provided to companies, according to the classification of the Catalogue of Economic Activities made known by the SAT through general rules and which are registered as border companies in terms of the Decree establishing the general import tax for the border region and the northern border strip.

For the purposes of this fraction, the following are considered as border strips and regions: the northern border strip adjacent to the United States of America, the southern border strip adjacent to Guatemala, the states of Baja California, Baja California Sur and Quintana Roo, the partial region of Sonora, and the municipalities of Caborca, Sonora, Cananea, Sonora, Salina Cruz, Oaxaca, Comitán de Domínguez, Chiapas and Tenosique, Tabasco.

The northern border strip adjacent to the United States of America is made up of the territory between the international dividing line in the north of the country and the parallel line at a distance of 20 kilometers toward the interior of the country, in the stretch between the limit of the partial region of the State of Sonora and the Gulf of Mexico, as well as the Border Municipality of Cananea, Sonora.

The southern border strip adjacent to Guatemala is the area covered by the 20 kilometer territory parallel to the international dividing line in the south of the country, in the stretch between the municipality of Unión Juárez and the mouth of the Suchiate River in the Pacific Ocean, within which the municipality of Tapachula, Chiapas, is located, with the corresponding geographical limits.

The partial region of the State of Sonora is comprised of the following limits: to the north, the international dividing line from the current course of the Colorado River to the point located on that line 10 kilometers west of Sonoyta, from that point, a straight line until reaching the coast, at a point located 10 kilometers east of Puerto Peñasco; from there, following the course of that river, northward until finding the international dividing line.

In order for the provisions of this section to be applicable, the following requirements must be met:

a) That the importer writes down in the import pedimento, before activating the automated selection mechanism, the key provided by the SHCP to identify the goods that are in the cases of this fraction, and

b) That the importer presents a declaration under protest of truth, indicating that the goods will comply with the commercial information requirements established in the NOMs NOM-004-SCFI-2006, NOM-015-SCFI-2007, NOM-020-SCFI-1997, NOM- 024-SCFI-2013, NOM-050-SCFI-2004, NOM-051-SCFI/SSA1-2010, NOM-186- SSA1/SCFI-2013, NOM-189-SSA1/SCFI-2002 and NOM-141-SSA1/SCFI-2012 under the terms of the simplified procedure issued for that purpose by the SE, through the General Directorate of Standards, which will not reissue them to the rest of the country, except under the terms and provisions established in said procedure and in the customs legislation.

Goods falling under tariff headings 1601.00.01, 1601.00.99, 1602.31.01, 1602.32.01, 1602.41.01, 1602.42.01, 1602.50.99, 1902.11.01, 1902.19.99,1902.20.01, 1902.30.99, 1905.31.01, 1905.32.01 and 9619.00.01 of the Tariff shall in no case qualify for the provisions of this heading.

- It is important to review the alternatives for the definitive import of goods that will undergo production processes, especially those that have been authorized by some sector of the Sectorial Promotion Programs.

- The reform of Annex 2.4.1 is intended to enter into force on October 1, 2020.

However, there are some exceptions to comply with the requirements of NOM-051-SCFI/SSA1-2010, which will be effective on April 1, 2021.

Therefore, it is recommended that foreign trade actors make representations to CONAMER if they consider that they may have an impact on the import procedures of their goods. Link: http://187.191.71.192/portales/resumen/49820

“In TLC Asociados, we develop a multidisciplinary team of experts in audits and risk analysis for consulting, implementing strategies and complying with foreign trade operations”.

For further information or comments regarding this article, please contact:

Consulting Division

TLC Asociados SC