Aviso de personal registrado ante el IMSS RECE: 22/LA

El 24 de diciembre de 2021 se dieron a conocer en el Diario Oficial de la Federación las “Reglas Generales de Comercio Exterior para 2022 y su anexo 13”, mismas que tuvieron vigencia al día 1 de enero de 2022, con excepción de los transitorios.

Posteriormente, el 11 de enero de 2022 se publicaron en el DOF los “Anexo 2 de las Reglas Generales de Comercio Exterior para 2022, publicadas el 24 de diciembre de 2021”, para entrar en vigor al día siguiente.

En este sentido, se identifican de forma general las nuevas obligaciones de las empresas con el Registro del Esquema de Certificación de Empresas(RECE):

I. Obligaciones de Empresas RECE

El Octavo Transitorio de las RGCE para 2022 incorporó una obligación para las empresas que cuentan con el Registro del Esquema de Certificación de Empresas, incluyendo aquellas que ingresaron una solicitud previa a la publicación de las nuevas disposiciones, de acuerdo con lo siguiente:[1]

“Octavo. Para efectos de cumplir con lo establecido en las reglas 7.1.1., primer párrafo, fracción III; 7.1.2., primer párrafo, fracción II, segundo párrafo, Apartado A, segundo párrafo, y cuarto párrafo; 7.1.3., primer párrafo, fracción I, inciso a) y fracción II, inciso a); 7.1.4., segundo párrafo, Apartado D, fracción IV, inciso a) y Apartado E, segundo párrafo, fracción I de la presente Resolución, se estará a lo siguiente:

I. Las empresas que cuenten con el Registro en el Esquema de Certificación de Empresas bajo las modalidades de IVA e IEPS, Operador Económico Autorizado y Socio Comercial Certificado, en cualquier rubro, vigente, que hayan obtenido su registro conforme al esquema de subcontratación establecido en los derogados artículos 15-A al 15-D de la Ley Federal del Trabajo, tendrán 15 días, contados a partir de la entrada en vigor de la presente Resolución, para informar a la AGACE mediante escrito libre de conformidad con la ficha de trámite 22/LA del Anexo 2, que cumplen con las reglas a que se refiere el primer párrafo de este transitorio, conforme al registro que tengan, debiendo adjuntar la documentación correspondiente. En caso contrario, se dará inicio a los procedimientos de requerimiento o cancelación del registro, establecidos en las reglas 7.2.2., 7.2.4. o 7.2.5., según corresponda.

II. Las empresas que antes de la entrada en vigor de la presente Resolución, hayan ingresado su “Solicitud de Registro en el Esquema de Certificación de Empresas”, tendrán 15 días contados a partir de la entrada en vigor de la misma, para cumplir con lo establecido en las reglas a que se refiere el primer párrafo de este transitorio, mediante escrito libre presentado ante la AGACE de conformidad con la ficha de trámite 22/LA del Anexo 2, con la información y documentación correspondiente a la solicitud del registro, en caso contrario la AGACE procederá conforme lo establecido en la regla 7.1.6.”

De lo anterior, se desprende los puntos que se indican:

- Los sujetos obligados son las empresas RECE que obtuvieron la autorización conforme al esquema de subcontratación, y las empresas que hayan solicitado el registro previo a la publicación de las RGCE para 2022.

- La empresa debe informar a la AGACE mediante escrito libre cumpliendo con los requisitos de la ficha de trámite 22/LA.

Cabe mencionar, que el Glosario de definiciones de las RGCE para 2022 menciona que el “Escrito libre” (19), es aquél que reúne los requisitos establecidos por los artículos 18 y 18-A del CFF, según corresponda y observa lo dispuesto en el artículo 19 del citado ordenamiento, así como en la regla 1.2.2

- El plazo es de presentación es de 15 días hábiles posteriores que deben computarse a partir del 1 de enero de 2022.

Es importante considerar únicamente los días hábiles conforme al artículo 12 del CFF, la regla 2.1.6 de la RMF para 2022, y el numeral 13 del Glosario definiciones de las RGCE para 2022.

- En el supuesto de no presentar el citado informe por parte de la empresa, la AGACE iniciará a los procedimientos de requerimiento o cancelación del registro, o al rechazo de la solicitud, según corresponda.[2]

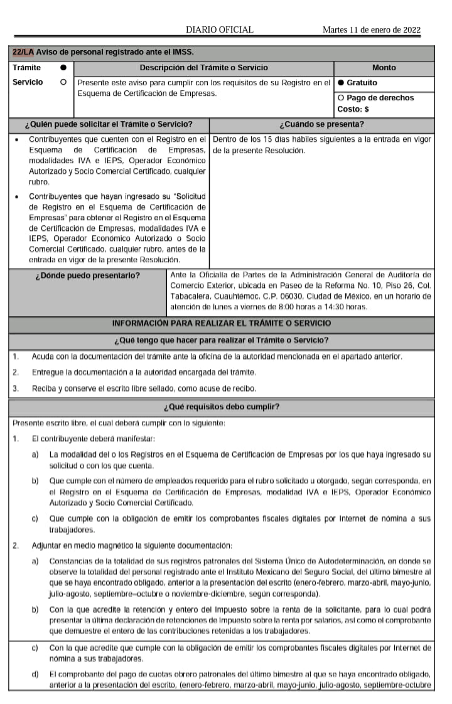

II. Ficha de Trámite 22/LA

Una vez que dio a conocer el formato se identifican algunas particulares que se indican a continuación:

- Es un trámite gratuito que se presenta ante la AGACE.

- ¿Quién puede solicitar el Trámite o Servicio?

- Contribuyentes que cuenten con el Registro en el Esquema de Certificación de Empresas, modalidades IVA e IEPS, Operador Económico Autorizado y Socio Comercial Certificado, cualquier rubro.

- Contribuyentes que hayan ingresado su “Solicitud de Registro en el Esquema de Certificación de Empresas” para obtener el Registro en el Esquema de Certificación de Empresas, modalidades IVA e IEPS, Operador Económico Autorizado o Socio Comercial Certificado, cualquier rubro, antes de la entrada en vigor de la presente Resolución.

Un aspecto relevante es que no hace una distinción sobre los sujetos obligados a la presentación del citado aviso.

- ¿Qué tengo que hacer para realizar el Trámite o Servicio?

- Acudir con la documentación del trámite ante la oficina de la autoridad.

- Entregue la documentación a la autoridad encargada del trámite.

- Reciba y conserve el escrito libre sellado, como acuse de recibo.

- ¿Qué requisitos debo cumplir?

Presente escrito libre, el cual deberá cumplir con lo siguiente:

- El contribuyente deberá manifestar:

a) La modalidad del o los Registros en el Esquema de Certificación de Empresas por los que haya ingresado su solicitud o con los que cuenta.

b) Que cumple con el número de empleados requerido para el rubro solicitado u otorgado, según corresponda, en el Registro en el Esquema de Certificación de Empresas, modalidad IVA e IEPS, Operador Económico Autorizado y Socio Comercial Certificado.

c) Que cumple con la obligación de emitir los comprobantes fiscales digitales por Internet de nómina a sus trabajadores.

- Adjuntar en medio magnético la siguiente documentación:

a) Constancias de la totalidad de sus registros patronales del Sistema Único de Autodeterminación, en donde se observe la totalidad del personal registrado ante el Instituto Mexicano del Seguro Social, del último bimestre al que se haya encontrado obligado, anterior a la presentación del escrito (enero-febrero, marzo-abril, mayo-junio, julio-agosto, septiembre–octubre o noviembre-diciembre, según corresponda).

b) Con la que acredite la retención y entero del Impuesto Sobre la Renta de la solicitante, para lo cual podrá presentar la última declaración de retenciones de Impuesto Sobre la Renta por salarios, así como el comprobante que demuestre el entero de las contribuciones retenidas a los trabajadores.

c) Con la que acredite que cumple con la obligación de emitir los Comprobantes Fiscales Digitales por Internet de nómina a sus trabajadores.

d) El comprobante del pago de cuotas obrero-patronales del último bimestre al que se haya encontrado obligado, anterior a la presentación del escrito, (enero-febrero, marzo-abril, mayo-junio, julio-agosto, septiembre-octubre o noviembre-diciembre, según corresponda), deberá adjuntar comprobante de pago descargado por el Sistema de pago referenciado o comprobante de pago que sea acorde con la información del Sistema Único de Autodeterminación. Aquellos comprobantes que contengan leyendas de que no tienen efectos fiscales o legales, no serán válidos para acreditar el requisito.

En resumen, las empresas relacionadas con esta obligación deberán cumplir en tiempo y forma con este informe con el objetivo de prevenir cualquier requerimiento o el inicio de un procedimiento de cancelación del registro por las autoridades.

Fuente de información:

http://dof.gob.mx/nota_detalle.php?codigo=5640445&fecha=11/01/2022

“En TLC Asociados desarrollamos un equipo multidisciplinario de expertos en auditorías y análisis de riesgos para asesorar y promover el cumplimiento en operaciones de comercio exterior”.

Para más información o comentarios sobre esta publicación contacte a:

División de Consultoría

TLC Asociados S.C.

Prohibida la reproducción parcial o total. Todos los derechos reservados de TLC Asociados, S.C. El contenido del presente artículo no constituye una consulta particular y por lo tanto TLC Asociados, S.C., su equipo y su autor, no asumen responsabilidad alguna de la interpretación o aplicación que el lector o destinatario le pueda dar.

[1] Nota: En las reglas 7.1.1, 7.1.2, 7.1.3 y 7.1.4 relacionadas con el Registro en el Esquema de Certificación de empresas se elimina la referencia del esquema de subcontratación de trabajadores vinculada con los artículos derogados 15-A al 15-D de la LFT.

[2] Cfr. Reglas 7.16, 7.2.2, 7.2.4 y 7.2.5 de las RGCE para 2022.

On December 24, 2021, the “General Rules for Foreign Trade for 2022 and their Annex 13” were published in the Official Gazette of the Federation, which entered into force on January 1, 2022, with the exception of the transitional provisions.

Subsequently, on January 11, 2022, the “Annex 2 of the General Foreign Trade Rules for 2022, published on December 24, 2021” was published in the Official Gazette of the Federation, to become effective the following day.

In this regard, the new obligations of companies with the Registration of the Company Certification Scheme (RECE) are generally identified:

I. Obligations of RECE Companies

The Eighth Transitory Provision of the RGCE (General Foreign Trade Rules) for 2022 incorporated an obligation for companies that have a Company Certification Scheme Registration, including those that filed an application prior to the publication of the new provisions, as follows:[1]

“Eighth Provision. For purposes of complying with the provisions of rules 7.1.1, first paragraph, section III; 7.1.2, first paragraph, section II, second paragraph, subsection A, second paragraph, and fourth paragraph; 7.1.3, first paragraph, section I, subsection a) and section II, subsection a); 7.1.4, second paragraph, subsection D, section IV, subsection a) and subsection E, second paragraph, section I of this Resolution, the following shall apply:

I. Companies Registered in the Company Certification Scheme under the VAT and STPS (Special Tax on Products and Services) modalities, as well as Authorized Economic Operator and Certified Business Partner, in any line of business, in force, that have obtained their registration under the subcontracting scheme established in the repealed Articles 15-A to 15-D of the Federal Labor Law, shall have 15 days starting from the entry into force of this Resolution, to notify the AGACE (General Administration of Foreign Trade Auditing), by means of free writing in accordance with form 22/LA in Annex 2, that they comply with the rules referred to in the first paragraph of this transitory provision, according to their registration, attaching the corresponding documentation. Otherwise, the procedures for the requirement or cancellation of the registration, established in rules 7.2.2, 7.2.4 or 7.2.5, as applicable, will be initiated.

II. Companies that prior to the entry into force of this Resolution, have filed their “Application for Registration in the Certification Scheme of Companies”, shall have 15 days from the entry into force of this Resolution, to comply with the provisions of the rules referred to in the first paragraph of this transitory provision, by means of a free writing submitted to the AGACE in accordance with the form 22/LA of Annex 2, with the information and documentation corresponding to the application for registration, otherwise the AGACE will proceed in accordance with the provisions of rule 7.1.6.”

From the foregoing, the following points can be inferred:

- The regulated entities are RECE companies that obtained authorization under the subcontracting scheme, and companies that have requested registration prior to the publication of the RGCE for 2022.

- The company must inform the AGACE by means of a free written document complying with the requirements of the procedure form 22/LA.

It is worth mentioning that the Glossary of definitions of the RGCE for 2022 mentions that the “Free writing” (19), is the one that meets the requirements established by articles 18 and 18-A of the Federal Tax Code, as applicable, and observes the provisions of article 19 of the aforementioned law, as well as rule 1.2.2.

- The deadline for filing is 15 working days from January 1, 2022.

It is important to consider only business days in accordance with article 12 of the Federal Tax Code, rule 2.1.6 of the Tax Miscellaneous Resolution for 2022, and paragraph 13 of the Glossary of definitions of the RGCE for 2022.

- In the event that the company does not submit the aforementioned report, the AGACE will initiate the procedures for the requirement or cancellation of the registration, or the rejection of the application, as the case may be.[2]

II. Form 22/LA

Once the format was released, some matters were identified as follows:

- It is a free procedure that is submitted to the AGACE.

- Who can request the Procedure or Service?

- Taxpayers that are registered in the Company Certification Scheme, VAT and STPS (Special Tax on Products and Services) modalities, Authorized Economic Operator and Certified Business Partner, any category.

- Taxpayers that have submitted their “Application for Registration in the Company Certification Scheme” to obtain Registration in the Company Certification Scheme, VAT and STPS (Special Tax on Products and Services) modalities, Authorized Economic Operator or Certified Business Partner, any category, prior to the entry into force of this Resolution.

A relevant aspect is that it does not distinguish between the parties obligated to file the aforementioned notice.

- What do I have to do to perform the Procedure or Service?

- Submit the documentation of the procedure to the authority’s office in person.

- Deliver the documentation to the authority in charge of the procedure.

- Receive and keep the sealed free writing, as acknowledgment of receipt.

- What are the requirements?

Submit a free writing, which must comply with the following

- The taxpayer shall state:

a) The type of Registration or Registrations in the Company Certification Scheme for which the application has been submitted or with which the application has been submitted.

b) The compliance with the number of employees required for the category requested or granted, as applicable, in the Registration in the Company Certification Scheme, VAT and STPS (Special Tax on Products and Services) modality, Authorized Economic Operator and Certified Business Partner.

c) The compliance with the obligation to issue payroll digital tax receipts via the Internet to its employees.

- Attach in magnetic media the following documentation:

a) Proof of the totality of the employer’s records of the Unified Self-determination System, where the totality of the personnel registered with the Instituto Mexicano del Seguro Social (Mexican Social Security Institute) for the last two-month period prior to the filing of the document (January-February, March-April, May-June, July-August, September-October or November-December, as applicable) is shown.

b) Documentation evidencing the applicant’s income tax withholding and payment, for which purpose the latest income tax withholding statement for salaries may be submitted, as well as proof of payment of the contributions withheld from the employees.

c) Documentation evidencing compliance with the obligation to issue Payroll Digital Tax Receipts via Internet to its employees.

d) The proof of payment of labor-employer dues for the last two-month period prior to the filing of the document (January-February, March-April, May-June, July-August, September-October or November-December, as the case may be), must be attached with proof of payment downloaded from the referenced payment system or proof of payment that is in accordance with the information of the Unified Self-determination System. Those receipts that contain legends that do not have fiscal or legal effects, will not be valid to accredit the requirement.

In summary, the companies related to this obligation must comply in due time and form with this report in order to prevent any requirement or the initiation of a registration cancellation procedure by the authorities.

Source:

http://dof.gob.mx/nota_detalle.php?codigo=5640445&fecha=11/01/2022

“In TLC Asociados, we develop a multidisciplinary team of experts in audits and risk analysis for consulting and ensuring compliance with foreign trade operations”.

For further information or comments regarding this article, please contact:

AEO and C-TPAT Certification Division

TLC Asociados S.C.

A total or partial reproduction is completely prohibited. All rights are reserved to TLC Asociados, S.C. The content of this article is not a consultation; therefore, TLC Asociados S.C., its team and its author do not assume any responsibility for the interpretations or implementations the reader may have.

[1] Note: In rules 7.1.1, 7.1.2, 7.1.3 and 7.1.4 related to the Registration in the Certification Scheme of companies, the reference to the subcontracting scheme of workers related to the repealed articles 15-A to 15-D of the LFT (Federal Labor Law) is eliminated.

[2] Cfr. Rules 7.16, 7.2.2, 7.2.4 and 7.2.5 of the RGCE (General Foreign Trade Rules) 2022.