AL12 – Cálculo de contribuciones y cuotas compensatorias por operaciones al amparo del procedimiento de revisión en origen/ Calculation of Contributions and Countervailing Duties for Operations under the Origin Review Procedure

En términos del artículo 99 de la Ley Aduanera y en relación directa con la regla 7.5.2, fracción VI de las Reglas Generales de Comercio Exterior para 2019, aquellas empresas que cuenten con el Registro de Despacho de Mercancías de las Empresas se encuentran obligadas a presentar el cálculo de contribuciones a más tardar el último día del mes de febrero de acuerdo al ejercicio inmediato anterior, tal y como se cita a continuación:

- Artículo 99. CÁLCULO DE CONTRIBUCIONES Y CUOTAS COMPENSATORIAS POR OPERACIONES AL AMPARO DEL PROCEDIMIENTO DE REVISIÓN EN ORIGEN Los importadores que realicen operaciones al amparo del procedimiento de revisión en origen calcularán, durante el mes de enero, las contribuciones y cuotas compensatorias que en los términos de este artículo deberán pagar por las importaciones efectuadas durante el ejercicio inmediato anterior, de acuerdo con lo siguiente: … Regla 7.5.2. OBLIGACIONES DE LAS EMPRESAS QUE CUENTEN CON EL REGISTRO DEL DESPACHO DE MERCANCíAS DE LAS EMPRESAS

Las empresas que hubieran obtenido la autorización en el Registro del Despacho de Mercancías de las Empresas, de conformidad con los artículos 98 y 100 de la Ley, 144 del Reglamento y la regla 7.5.1., estarán sujetas al cumplimiento permanente de las siguientes obligaciones:

…VI. Para efectos de lo señalado en el artículo 98, fracción IVde la Ley, las empresas que hayan obtenido su inscripción en el registro del despacho de mercancías de las empresas deberán presentar, a través de Ventanilla Digital a más tardar el último día de febrero de cada año, el cálculo a que se refiere el artículo 99 de la Ley correspondiente al ejercicio inmediato anterior y, en su caso, la copia del comprobante con el que acrediten el pago realizado del monto total de contribuciones y, en su caso, cuotas compensatorias que resulte en los términos del artículo 99, fracción III de la Ley.

…”

Para la realización del cálculo, se procederá de acuerdo con lo siguiente:

Fracción I:

Monto total de contribuciones y cuotas compensatorias pagadas por el importador de manera espontánea, conforme a la fracción V del artículo 98 de esta Ley, en el ejercicio inmediato anterior.

CE = $ XXXXXX.XX

Monto total de contribuciones y cuotas compensatorias declaradas por el importador en los pedimentos que no fueron objeto de reconocimiento aduanero, verificación de mercancías en transporte o visitas domiciliarias en el ejercicio inmediato anterior.

CDV = $ XXXXXX.XX

ME = Margen de error = X.XX

Fracción II:

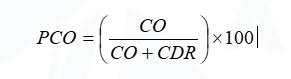

Monto total de las contribuciones y cuotas compensatorias omitidas detectadas con motivo del reconocimiento aduanero, segundo reconocimiento, verificación de mercancías en transporte o visitas domiciliarias en el ejercicio inmediato anterior.

CO = $ XXXXXX.XX

Monto total de contribuciones y cuotas compensatorias declaradas por el importador en los pedimentos que fueron objeto de reconocimiento aduanero, segundo reconocimiento, verificación de mercancías en transporte o visitas domiciliarias en el ejercicio inmediato anterior.

CDR = $ XXXXXX.XX

PCO= Porcentaje de contribuciones y cuotas compensatorias omitidas = 0

Fracción III:

Si el porcentaje obtenido en el cálculo de la fracción II es mayor al ME, el porcentaje excente se aplicará al total de contribuciones y CO pagadas que no fueron objeto de reconocimiento aduanero, verificación de mercancías en transporte o visitas domiciliarias, incluyendo las contribuciones y cuotas compensatorias pagadas espontáneamente.

(PCO-ME/100) X (CDV+CE)

El monto total de contribuciones y cuotas compensatorias que resulte en los términos de esta fracción se pagará a más tardar el día 17 del mes de febrero del año siguiente del ejercicio que se determina.

Ahora bien, si el porcentraje es menor, se declara que el PCO no es mayor que ME.

Fracción IV:

Si el PCO es igual o menor al ME calculados en términos de la fraccón I y II, no habrá lugar al pago de contribuciones o de cuotas compensatorias.

Dicho lo anterior, es importante que se cumpla con la obligación apuntada en el artículo 99 de la Ley Aduanera y la regla 7.5.2 fracción VI de las Reglas Generales de Comercio Exterior para 2019.

La omisión de la presentación del cálculo de contribuciones ante la Autoridad sería causal de suspensión del registro, en términos de la regla 7.5.5 fracción III de las RGCE para 2019.

“En TLC Asociados desarrollamos un equipo multidisciplinario de expertos en auditorías y análisis de riesgos para asesorar, implementar estrategias y dar cumplimiento en operaciones de comercio exterior”.

Para más información o comentarios sobre esta publicación contacte a:

División Legal

TLC Asociados S.C.

Prohibida la reproducción parcial o total. Todos los derechos reservados de TLC Asociados, S.C. El contenido del presente artículo no constituye una consulta particular y por lo tanto TLC Asociados, S.C., su equipo y su autor, no asumen responsabilidad alguna de la interpretación o aplicación que el lector o destinatario le pueda dar.

In terms of article 99 of the Customs Law and with direct relation to rule 7.5.2, section VI of the General Rules of Foreign Trade for 2019, those companies that have the Registry of Merchandise Dispatch of Companies are obliged to present the calculation of contributions no later than the last day of the month of February according to the immediately preceding fiscal year, as quoted below:

- Article 99. CALCULATION OF CONTRIBUTIONS AND COUNTERVAILING DUTIES FOR OPERATIONS UNDER THE ORIGIN REVIEW PROCEDURE Importers conducting operations under the origin review procedure shall calculate, during the month of January, the contributions and countervailing duties to be paid under the terms of this Article on imports during the previous fiscal year, in accordance with the following: … Rule 7.5.2. OBLIGATIONS FOR COMPANIES WITH REGISTRATION OF THE DISPATCH OF GOODS OF COMPANIES

The companies that have obtained the authorization in the Registry of the Dispatch of Goods of the Companies, in accordance with articles 98 and 100 of the Law, 144 of the Regulation and rule 7.5.1:

…VI. For the purposes of the provisions of article 98, section IV of the Law, the companies that have obtained their registration in the registry of the dispatch of goods of the companies, must present through the Digital Window no later than the last day of February of each year, the calculation referred to in article 99 of the Law, corresponding to the immediately preceding fiscal year and, if applicable, the copy of the voucher with which they accredit the payment made of the total amount of contributions and, if applicable, countervailing duties resulting in the terms of article 99, section III of the Law.

…”

The calculation shall be carried out in accordance with the following:

Section I:

Total amount of contributions and countervailing duties paid by the importer spontaneously, in accordance with section V of Article 98 of this Law, in the immediately preceding fiscal year.

CE = $ XXXXXX.XX

Total amount of contributions and countervailing duties declared by the importer on pedimentos that were not subject to customs examination, verification of goods in transport or home visits in the immediately preceding fiscal year.

CDV = $ XXXXXX.XX

Section II:ME = Margin of error = X.XX

Total amount of contributions and countervailing duties omitted on the occasion of customs examination, second examination, verification of goods in transport or home visits in the immediately preceding year.

CO = $ XXXXXX.XX

Total amount of contributions and countervailing duties declared by the importer on the pedimentos that were subject to customs examination, second examination, verification of goods in transport or home visits in the immediately preceding fiscal year.

CDR = $ XXXXXX.XX

PCO= Percentage of omitted contributions and countervailing duties = 0

Fracción III:

If the percentage obtained in the calculation of section II is greater than the ME, the excess percentage shall be applied to the total contributions and CO paid that were not subject to customs examination, verification of goods in transport or home visits, including contributions and countervailing duties paid spontaneously.

(PCO-ME/100) X (CDV+CE)

The total amount of contributions and countervailing duties resulting from the terms of this section shall be paid no later than the 17th day of February of the year following the year to be determined.

However, if the percentage is lower, it is declared that the PCO is not greater than ME.

Section IV:

If the PCO is equal to or less than the ME calculated in terms of Fractions I and II, there will be no place for the payment of contributions or countervailing fees.

Having said that, it is necessary to comply with the obligation indicated in Article 99 of the Customs Law and Rule 7.5.2 section VI of the General Rules of Foreign Trade for 2019.

The omission of the presentation of the calculation of contributions before the Authority, would be cause for suspension from the registration in term of rule 7.5.5 section III of the RGCE for 2019.

“In TLC Asociados, we develop a multidisciplinary team of experts in audits and risk analysis for consulting, implementing strategies and complying with foreign trade operations”.

For further information or comments regarding this article, please contact:

Legal Division

TLC Asociados S.C.

A total or partial reproduction is completely prohibited. All rights are reserved to TLC Asociados, S.C. The content of this article is not a consultation; therefore, TLC Asociados S.C., its team and its author do not assume any responsibility for the interpretations or implementations the reader may have.

.