3a Resolución de Modificaciones de las Reglas Generales de Comercio Exterior para 2020

El 22 de diciembre de 2020 fue publicada en el DOF la “Tercera Resolución de Modificaciones a las Reglas Generales de Comercio Exterior para 2020”, la cual tendrá vigencia el 28 de diciembre de 2020, con excepción de los transitorios.

En este apartado se identificarán las principales adiciones y reformas, mismas que se indican a continuación:

I. Cambios de las disposiciones generales

1) Son reformadas 63 reglas, adicionadas 7 reglas, derogadas 2 reglas y reformados 19 anexos.

2) En términos generales, en las disposiciones se introduce el elemento del NICO en las referencias de la clasificación arancelaria o citas de fracciones arancelarias.

3) También se realizan algunas precisiones de redacción para hacerlas comprensibles.

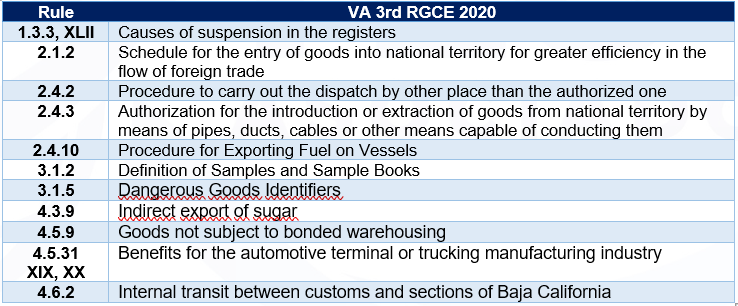

II. Causales de suspensión en los padrones

1) Regla 1.3.3 de las RGCE 2020.

2) La fracción VII hace precisiones de la conjunción “o”.

3) La fracción XXIV hace referencia a la nueva “Ley Federal de Protección a la Propiedad Industrial” antes “Ley de la Propiedad Industrial.

4) La fracción XXIX precisa cuando se esté sujeto a las facultades de comprobación.

5) La fracción XL deja de mencionar la “mercancía que se clasifique en alguna de las fracciones arancelarias listadas en el Sector 13” y solo indica la” mercancía señalada”.

6) La fracción XLII incluye el término de los números de identificación comercial y la clasificación arancelaria de las mercancías relacionadas con el sector 9.

7) La fracción XLIII deja de mencionar las “mercancías clasificadas en las fracciones arancelarias señaladas en el Anexo 10” y solo indica las” mercancías señaladas”.

8) La fracción XLIV hace referencia al término completo “régimen aduanero de depósito completo”.

9) La fracción XLV adiciona el supuesto “cuando hayan realizado operaciones con personas físicas o morales que se encuentren publicadas en el listado mencionado, sin haber acreditado que efectivamente adquirieron los bienes o recibieron los servicios amparados con los comprobantes fiscales correspondientes o, en su caso, no hubieran corregido su situación fiscal, en términos de los párrafos octavo y noveno del referido artículo”.

III. Reincorporación en los Padrones

1) Regla 1.3.4 de las RGCE 2020.

2) Precisa el inicio de PAMA o levantamiento de un acta circunstanciada de hechos u omisiones.

3) Ahora indica la presentación de un escrito libre en el que se manifieste expresamente el allanamiento a la irregularidad detectada o determinación correspondiente.

IV. Procedimiento para dejar sin efectos la suspensión para operar en el SEA

1) Regla 1.4.15 de las RGCE 2020.

2) Se adiciona el procedimiento para dejar sin efectos la suspensión para operar en el SEA por la declaración inexacta del NICO para mercancía sensibles del textil, calzado y vehículos usados.

3) Opción de desvirtuar el causal o presentar la CAG mediante pedimento R1.

4) Dar aviso a la autoridad aduanera para que, en caso de ser procedente, active el sistema en un plazo de 5 DH.

5) Cumplir con ficha de trámite 146/LA

V. Pago del aprovechamiento de los autorizados para prestar los servicios de pre validación electrónica

1) Regla 1.8.3 de las RGCE 2020.

2) Deja de referir “el fideicomiso público a que se refiere el artículo 16-A de la Ley, a través de la TESOFE”, debido que fueron eliminados los Fideicomisos en la reforma a la Ley Aduanera el 6 de noviembre de 2020.

VI. Diferencias de clasificación arancelaria en los certificados o certificaciones de origen.

1) Regla 3.1.12 de las RGCE 2020.

2) Incorpora los documentos de prueba de origen y la certificación de origen adicionales al certificado de origen.

VII. Pedimento consolidado con relación del CFDI o documentos equivalentes

1) Regla 3.1.25. de las RGCE 2020.

2) Modifica la estructura de la disposición en donde el último párrafo lo incorpora en la fracción III.

VIII. Casos en los que no se está obligado al pago del DTA

1) Regla 5.1.2. de las RGCE 2020.

2) Se precisa la referencia de la regla 3.1.21., fracción III, inciso b).

IX. Rectificación de Pedimentos

1) Regla 6.1.1 de las RGCE 2020.

2) Se modifica la excepción del requisito de la rectificación relacionada cuando se declare una nueva tasa TIGIE, incluso cuando cambien la clasificación arancelaria.

3) Se adicionan requisitos para solicitar autorización de la R1, que el interesado cumpla con sus obligaciones fiscales, no estar publicado como empresas inexistentes por el SAT, el domicilio debe estar localizado en el RFC y contar con buzón tributario.

4) La autoridad aduanera podrá requerir al solicitante otorgado un plazo de 10 DH y, en caso de no atender al requerimiento, se tendrá por no presentado.

X. Rectificación para solicitar trato arancelario preferencial después de la importación de mercancías

1) Regla 6.1.4 de las RGCE 2020.

2) Se incorpora la obligación de anexar al pedimento la declaración de origen cuando se realice la rectificación para aplicar preferencias arancelarias posterior al cruce de las mercancías, es decir, con el objetivo de aplicar retroactivamente los aranceles preferenciales.

3) Adicionalmente, deberá declararse el identificador “TL” y demás claves, según corresponda.

XI. Requisitos para obtener la CIVA la modalidad de IVA e IEPS, rubro A

1) Regla 7.1.2 de las RGCE 2020.

2) Se precisa la referencia del “retorno” en forma general y deja de mencionar “retorno al extranjero”.

XII. Beneficios de las empresas que cuenten con el RECE en la modalidad de OEA

1) Regla 7.3.3 de las RGCE 2020.

2) La fracción XXIII deja de hacer referencia a la ACOP y ahora menciona a la AGSC.

3) La fracción XXVII precisa la referencia de la regla 3.1.21., fracción III, inciso b).

XIII. Procedimiento para efectuar el despacho por lugar distinto al autorizado

1.Regla 2.4.2 de las RGCE para 2020.

2. En la fracción I, incisos a) y b) se incorporan las fracciones arancelarias y el NICO.

3. En la fracción III, inciso a) se adiciona la referencia a la fracción arancelaria y el número de identificación comercial.

4. En la fracción III, inciso f) se incorporan las fracciones arancelarias y el NICO.

XIV. Autorización para despacho por lugar distinto al autorizado en embarcaciones

1.Regla 2.4.13 de las RGCE para 2020.

2. Se reorganiza la estructura de la disposición en general.

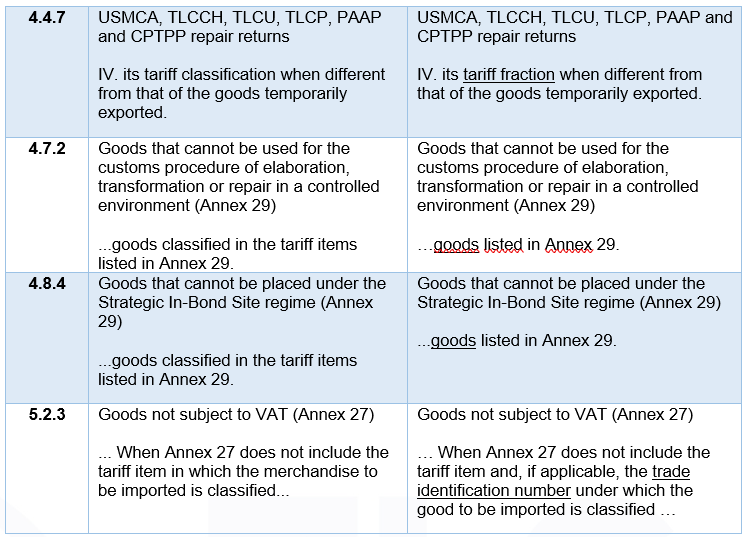

XV. Modificaciones de algunas disposiciones para hacer referencia al NICO o deja de referir a la fracción arancelaria.

XVI. Disposiciones que en su texto sustituyen la referencia de la fracción arancelaria a 8 dígitos para incluir la clasificación arancelaria junto con el NICO

“En TLC Asociados desarrollamos un equipo multidisciplinario de expertos en auditorías y análisis de riesgos para asesorar y dar cumplimiento en operaciones de comercio exterior”.

Para más información o comentarios sobre esta publicación contacte a:

División de Consultoría

TLC Asociados SC

Prohibida la reproducción parcial o total. Todos los derechos reservados de TLC Asociados, S.C. El contenido del presente artículo no constituye una consulta particular y por lo tanto TLC Asociados, S.C., su equipo y su autor, no asumen responsabilidad alguna de la interpretación o aplicación que el lector o destinatario le pueda dar.

On December 22 of 2020, the “Third Resolution of Amendments to the General Rules of Foreign Trade for 2020” was published in the Official Journal of the Federation, which will be valid as of December 28, 2020, except for the transitory articles.

This section will identify the main additions and amendments, which are indicated below:

I. Changes to General Provisions

1) About 63 rules are reformed, 7 rules are added, 2 rules are repealed and 19 annexes are amended.

2) In general terms, the provisions introduce the NICO element in the tariff classification references or tariff item quotes.

3) Some editorial clarifications are also made to make them understandable.

II. Causes of suspension from the registers

1) Rule 1.3.3 of the RGCE 2020.

2) Section VII clarifies the conjunction “or”.

3) Section XXIV refers to the new “Federal Law for the Protection of Industrial Property” formerly “Industrial Property Law”.

4) Section XXIX indicates when you are subject to the faculties of verification.

5) Section XL no longer mentions the “good that is classified in any of the tariff sections listed in Sector 13” and only indicates the “marked good”.

6) Section XLII includes the term of the trade identification numbers and the tariff classification of goods related to sector 9.

7) Section XLIII no longer mentions the “goods classified in the tariff items listed in Annex 10” and only indicates the “marked goods“.

8) Section XLIV refers to the full term “full customs warehousing regime“.

9) Section XLV adds the case “when they have carried out transactions with individuals or corporations that are published in the aforementioned list, without having proven that they actually acquired the goods or received the services covered by the corresponding tax vouchers or, if applicable, had not corrected their tax situation, in terms of the eighth and ninth paragraphs of the aforementioned article“.

III. Reincorporation in the Registers

1) Rule 1.3.4 of the RGCE 2020.

2) Specifies the beginning of PAMA or the drawing up of a circumstantial record of facts or omissions.

3) Now it indicates the presentation of a free writing in which the invasion to the detected irregularity or corresponding determination is expressly manifested.

IV. Procedure for lifting the suspension to operate in the Customs Electronic System (SEA)

1) Rule 1.4.15 of the RGCE 2020.

2) The procedure is added to render the suspension ineffective for operating in the SEA due to the inaccurate declaration of the NICO for sensitive textile, footwear and used vehicle goods.

3) Option of denying the cause or presenting the CAG through pedimento R1.

4) Give notice to the customs authority so that, if appropriate, it activates the system within 5 working days.

5) Fulfill the form 146/Customs Law

V. Payment for the use of those authorized to provide electronic pre-validation services

1) Rule1.8.3 of the RGCE 2020.

2) It no longer refers to “the public trust referred to in Article 16-A of the Law, through the TESOFE”, because the Trusts were eliminated in the reform to the Customs Law on November 6, 2020.

VI. Differences in tariff classification in certificates or certifications of origin

1) Rule 3.1.12 of the RGCE 2020.

2) Incorporates additional proof of origin documents and certification of origin into the certificate of origin.

VII. Consolidated Pedimento in relation to the CFDI or equivalent documents

1) Rule 3.1.25. of the RGCE 2020.

2) Modifies the structure of the provision where the last paragraph incorporates it in section III.

VIII. Cases in which you are not required to pay DTA

1) Rule 5.1.2. of the RGCE 2020.

2) The reference in Rule 3.1.21., section III, paragraph b) is specified.

IX. Rectification of Pedimentos

1) Rule 6.1.1 of the RGCE 2020.

2) The exception from the requirement of the related rectification is modified when a new TIGIE rate is declared, even when the tariff classification changes.

3) Requirements are added to request authorization of R1, that the interested party comply with its tax obligations, not be published as non-existent companies by SAT, the address must be located in the RFC and have a tax mailbox.

4) The customs authority may request the applicant to be granted a term of 10 working days and, in case of not attending the request, it will be considered as not having been presented.

X. Rectification to apply for preferential tariff treatment after the import of goods

1) Rule 6.1.4 of the RGCE 2020.

2) It incorporates the obligation to attach to the pedimento the declaration of origin when the correction is made to apply tariff preferences after the goods have been crossed, that is, with the objective of retroactively applying the preferential tariffs.

3) Additionally, the identifier “TL” and other keys must be declared, as applicable.

XI. Requirements to obtain the VAT Certification in the modality of VAT and STPS, item A

1) Rule 7.1.2 of the RGCE 2020.

2) The reference to “return” in a general way is clarified and no longer mentions “return abroad”.

XII. Benefits of the companies that have the RECE in the modality of AEO

1) Rule 7.3.3 of the RGCE 2020.

2) Section XXIII no longer refers to the ACOP and now mentions the AGSC.

3) Section XXVII specifies the reference of rule 3.1.21., section III, paragraph b).

XIII. Procedure to carry out the dispatch by other place than the authorized one

1) Rule 2.4.2 of the RGCE for 2020.

2) In section I, paragraphs a) and b), the tariff and NICO sections are incorporated.

3) In section III, subsection a) the reference to the tariff section and the commercial identification number are added.

4) Section III, subsection f) includes the tariff sections and the NICO.

XIV. Authorization for dispatch by different place than the one authorized in boats

1) Rule 2.4.13 of the RGCE for 2020.

2) The overall layout structure is reorganized.

XV. Modification of some provisions to refer to the NICO or no longer refer to the tariff item

XVI. Provisions that in its text replace the reference of the 8-digit tariff item to include the tariff classification together with the NICO

“In TLC Asociados, we develop a multidisciplinary team of experts in audits and risk analysis for consulting and ensuring compliance with foreign trade operations”.

For further information or comments regarding this article, please contact:

Consulting Division

TLC Asociados SC

A total or partial reproduction is completely prohibited. All rights are reserved to TLC Asociados, S.C. The content of this article is not a consultation; therefore, TLC Asociados S.C., its team and its author do not assume any responsibility for the interpretations or implementations the reader may have.